Weekly macroeconomic and market update 21 December 2015

Weekly macroeconomic and market update

The most discussed economic event of the year

Arguably the most discussed economic event of the year came to pass with the US Fed raising interest rates for the first time since 2006, although given the sensitivities, the Fed did exactly what everyone expected – a 25 bps hike to give a new ‘corridor’ of 0.25-0.50% for the Fed Funds rate. The messaging remained to expect a very gradual hike, and almost to highlight the point, some of the rate path forecasts in the years ahead were reported as more dovish – however the decision to hike rates was unanimous. Equity markets initially rallied during the press conference, but subsequently slid through the rest of the week. Our house view remains that this has come too late in the cycle and we remain particularly concerned about US markets.

Surprise moves from the Bank of Japan

Hot on the heels of the Fed action, the Bank of Japan surprised markets by appearing to join the ECB in loosening monetary policy whilst denying any fresh stimulus and referring to the changes as technicalities. The move, which was only supported by a 6-3 decision, will see the Bank of Japan purchase longer-dated bonds (seven to twelve years, from seven to ten previously) – and also increase the equity purchase programme by purchasing a further 300 billion yen (equivalent to US$2.4 billion) of equity.

Confusingly, however, this equity is reportedly to be targeted at companies proactively investing in labour and capex, though the details remain vague. Overall this surprise move caught markets off guard and it doesn’t appear to have been well executed, which could sap the Japanese authorities’ credibility.

Growing support for Spain’s anti-austerity party

It was a bad week for traditional political parties in Spain as the conservative Prime Minister Mariano Rajoy lost his majority and anti-austerity parties received a lot of support. The ruling People’s Party was still the largest party, but remains far short of a majority with 29% of the vote. The main opposition Socialist party received 22% but it was the anti-austerity Podemos party that did even better than expected, receiving 21% of the vote. The political mathematics now starts, but with the latest disruption and disparate political stances, it is currently difficult to see how a stable and enduring coalition could work.

Revised Chinese GDP expectations for next year

Chinese authorities are expecting GDP growth of 6.8% in 2016 – a slowdown from official estimates of 6.9% this year, and still far more optimistic than most other observers. The revised figures represent official acknowledgement of the growing problems facing the world’s second largest economy, with recognition that rising non-performing loans and overcapacity would hamper the economy – though the Peoples’ Bank of China also believes stimulus and reform measures will offset much of these drags. Also on China it is noteworthy that, following last week’s announcement of the change to how the currency would be valued and the action of the US Fed, the renminbi depreciated slightly against the US dollar through last week.

Last week’s other events

The markets

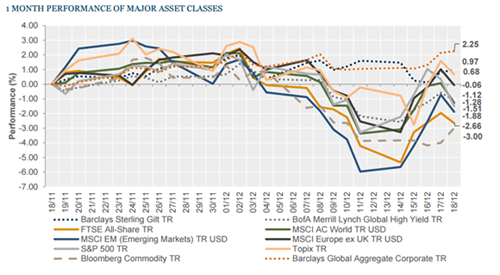

Equity and bond markets remain mixed in relatively thin trading, with the US rally after the Fed announcement quickly fading amid another difficult week for oil.

The week ahead

With the Christmas period upon us, there is relatively little in the way of data out over the next couple of weeks. On Wednesday the UK releases Q3 GDP figures which are likely to be confirmed as 2.4% year on year, and then the US gives us the usual data dump of inflation durable goods, personal spending and home sales. Given the volatility in the oil price, the weekly EIA Crude Oil Stocks readings are likely to be closely watched and could drive some market volatility. New Year’s Day will see Chinese official PMI for both manufacturing and non-manufacturing.

This article was previously published on Tilney prior to the launch of Evelyn Partners.

Some of our Financial Services calls are recorded for regulatory and other purposes. Find out more about how we use your personal information in our privacy notice.

Your form has been submitted and a member of our team will get back to you as soon as possible.

Please complete this form and let us know in ‘Your Comments’ below, which areas are of primary interest. One of our experts will then call you at a convenient time.

*Your personal data will be processed by Evelyn Partners to send you emails with News Events and services in accordance with our Privacy Policy. You can unsubscribe at any time.

Your form has been successfully submitted a member of our team will get back to you as soon as possible.