Investment Outlook: Pump up the valuations

A monthly round-up of global markets and trends

A monthly round-up of global markets and trends

Equity valuations are generally led by accommodative monetary policy and robust US economic growth. These drive money into the market and boosts corporate earnings. Although risks persist (and particularly in the Middle East), historical patterns indicate that the current backdrop is conducive to further valuation expansion, suggesting potential for equities to continue to rise in 2026.

Some may remember the late 1980s dance classic Pump Up the Volume by MARRS, a track that evokes visions of glow sticks, neon colours and sticky club floors. For others, it is simply a reminder of an era defined by synthesizers and questionable fashion choices. But today’s financial markets aren’t pumping up the volume, they are pumping up the valuations.

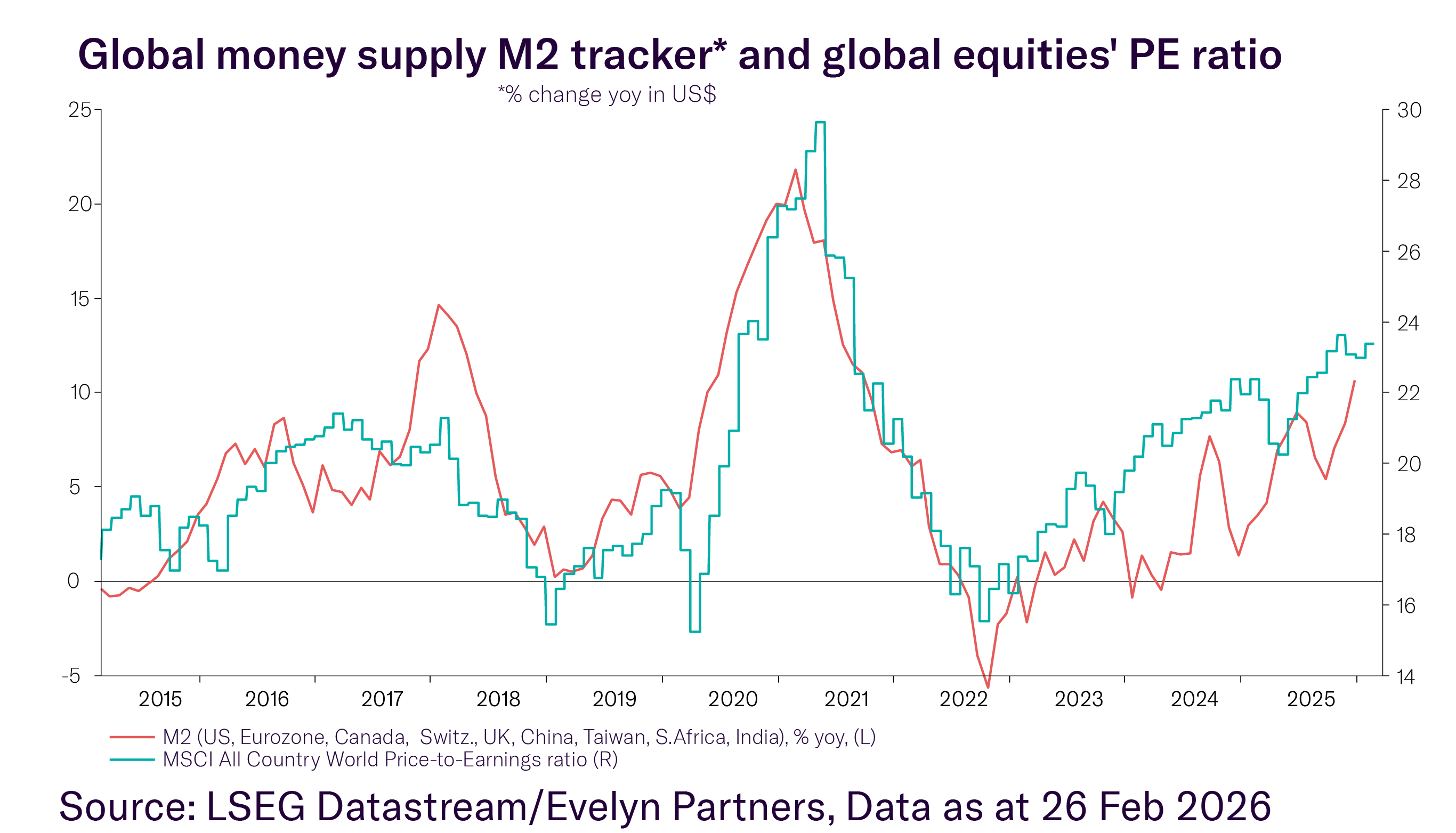

Historically, share prices are supported by two forces that lift valuation multiples: accommodative monetary policy and solid economic growth. When these conditions occur together, especially alongside strong earnings growth, they often create a powerful backdrop for equity returns.

Fiscal and monetary policy are working together to expand the money flowing around the financial system. The shift began with central banks. In March 2024, the Swiss National Bank became the first major developed market central bank to cut interest rates, and this set off a broader pivot. The European Central Bank, the Bank of England and eventually the US Federal Reserve (Fed) followed with their own rate cuts.

Central bank balance sheets have also played a significant role. After more than a year of quantitative tightening (QT, or a shrinking of a central bank’s balance sheet), the Fed reversed course late last year. By December, it had stopped QT and resumed balance‑sheet expansion, adopting a lighter form of quantitative easing (QE) focused on buying short‑dated Treasuries at roughly $40 billion per month. While this approach does not suppress long‑term yields as earlier QE programmes did, it still injects money into the financial system.

Commercial banks also create money by extending loans. Over the past year, loan growth has risen, supported by lower interest rates and easier credit conditions. This expansion in money supply tends to increase equity valuations.

However, there is some uncertainty around how President Donald Trump’s Fed Chair nomination, Kevin Warsh, may approach future monetary policy. But for now, the direction is clear: balance sheets are expanding, and financial conditions remain loose.

Monetary support tells only part of the story. The second major driver of valuation expansion is solid economic growth. On that front, the US continues to perform strongly. The Atlanta Fed estimates first quarter 2026 real GDP at 3%, following a 1.4% actual print in the previous quarter.1

Growth is being driven by resilient private consumption and a surge in investment, particularly in digital infrastructure and data centres. In the fourth quarter of 2025, Microsoft doubled its capital expenditure to $30 billion, while Alphabet announced a remarkable $175-$185 billion capex plan for 2026 (nearly double its 2025 levels), aimed at AI compute capacity, DeepMind training clusters and cloud infrastructure.1

Market indicators echo this resilience. The US yield curve, measured by the spread between the 10-year and 2-year Treasury yields, has begun to steepen. This signal has been closely correlated with the manufacturing ISM and suggests stronger economic growth in the quarters ahead. This steepening suggests that recession odds are falling and that growth may continue to surprise to the upside.

To estimate potential equity returns, we analyse how valuation multiples respond to the interaction of Fed monetary policy with US economic growth, using data extending back to 1980. Two variables matter most:

For our analysis, we define growth as accelerating when real GDP exceeds 2%, stable when it ranges between 0 and 2%, and contracting when it turns negative. Fed policy is described as cutting, stable or raising rates based on the fed funds rate relative to its 12-month average.

Historically, the most supportive environment for valuation expansion occurs when growth is stable or accelerating and interest rates are stable or falling. Under these conditions, price earnings (PE) ratios have typically increased over the following year. Today's environment fits the combination of accelerating growth and rate cuts. The futures markets are currently pricing around 75 basis points of interest rate cuts over the next year.1 Historically, this combination has been associated with a nearly 18% PE ratio expansion.

This compares to less favourable environments that show weaker effects. When growth is contracting and the Fed is raising interest rates, PE ratios have risen by only around 0.9%1. The most challenging scenario occurs when the Fed cuts rates because growth is deteriorating, a situation markets often interpret as policy makers falling behind the curve. In these cases, PE ratios have historically fallen by as much as 8%.1

By pairing these valuation patterns with EPS expectations and current forward PE of 22 times, it is possible to sketch potential S&P 500 outcomes for end 2026:

Global equity valuations today sit above their long‑term averages, although still below the extremes of the dot‑com era. Investors are concerned that valuations could return to their long run historical norms and drag down returns.

However, a recent Minneapolis Fed study challenges this idea.2 The authors argue that when labour’s share of income falls and free cash flow rises, as has been the trend for decades, valuation multiples can rise and stay elevated. This pattern aligns with long term structural shifts, including the growth of the internet, China’s entry into the World Trade Organization, widespread offshoring, automation and now generative AI. All have weakened labour’s pricing power and pushed labour compensation as a share of GDP to historic lows.

Over the long run, the biggest risk is political. A populist shift that redirects income back toward labour could compress profit margins and valuation multiples. For now, however, there is no clear catalyst for such a shift.

With accommodative policy and solid growth working together, there is a supportive backdrop for valuation expansion. While market risks remain, with events in the Middle East a stark reminder, the balance of probabilities points to further upside for equities, supported by strong earnings resilience, abundant market liquidity and low recession risk. Markets may not be ready to pump up the volume, but they certainly appear positioned to pump up the valuations.

1 LSEG, Evelyn Partners

2 Federal Reserve bank of Minneapolis, A Macroeconomic Perspective on Stock Market Valuation Ratios, January 2026

Some of our Financial Services calls are recorded for regulatory and other purposes. Find out more about how we use your personal information in our privacy notice.

Your form has been submitted and a member of our team will get back to you as soon as possible.

Please complete this form and let us know in ‘Your Comments’ below, which areas are of primary interest. One of our experts will then call you at a convenient time.

*Your personal data will be processed by Evelyn Partners to send you emails with News Events and services in accordance with our Privacy Policy. You can unsubscribe at any time.

Your form has been successfully submitted a member of our team will get back to you as soon as possible.