Has gold outlived its usefulness as a hedge?

Our take: gold is an imperfect hedge, but the long-term case for owning remains intact

Our take: gold is an imperfect hedge, but the long-term case for owning remains intact

Historically, the price of gold has been driven by:

Its store of value: when investors worry about inflation, weak currencies, or high government borrowing they turn to gold for its perceived ability to preserve purchasing power.

A weaker dollar: Gold is typically priced in dollars, so a weaker dollar tends to support the price, especially for non-US dollar buyers.

Interest rates: Matter as gold pays no income, so when cash and bonds offer high real returns (after inflation) or rates are expected to rise, gold can look less attractive and vice versa.

Breadth of demand: Interest in gold is broad and diversified, driven by central banks, institutional and retail investors, jewellery consumption and industrial / technology use.

Constrained supply: Despite the best mining efforts, supply is slow to respond to rising demand

Portfolio diversifiication: Gold has often acted as a safe-haven in times of economic, monetary and geopolitical volatility and behaves differently to traditional equities and bonds.

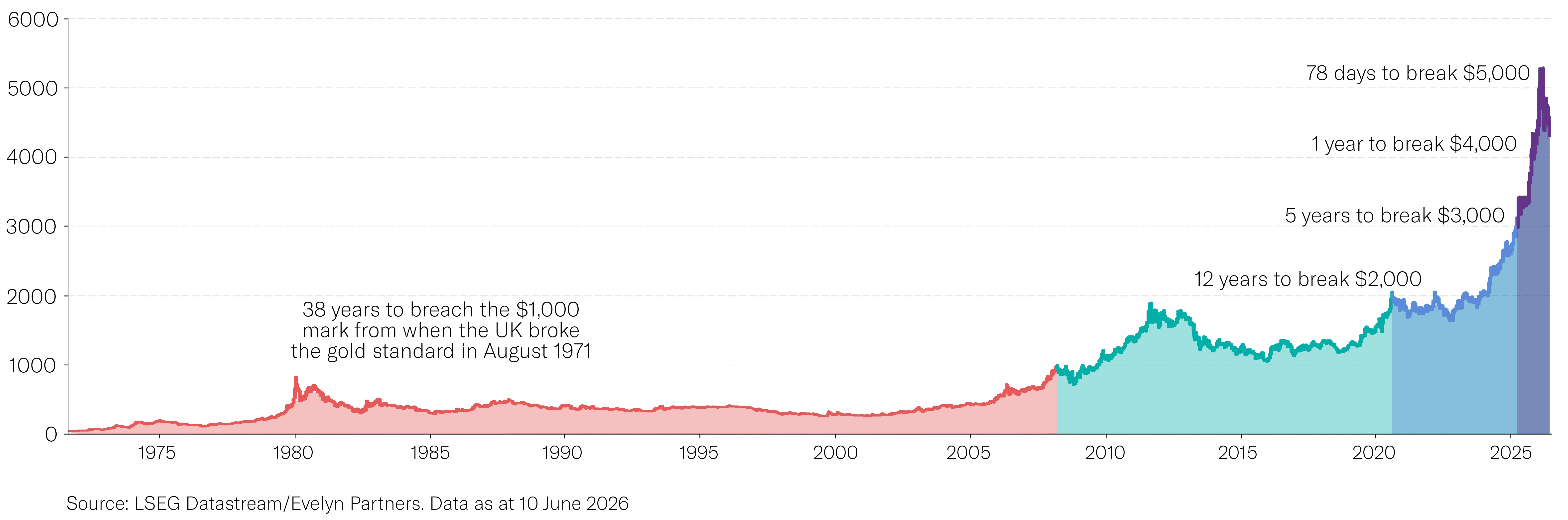

In the early part of 2026, the long-term gold story experienced a short-term reversal. Gold encountered a "perfect storm" after a strong two-year rally. Such strong performance over such a short timeframe made gold technically overbought (figure 1). When combined with a sudden shift in US interest rate expectations from cuts to hikes and central banks pausing their purchases meant marginal buyers were replaced with marginal sellers which weighed on returns over the year.

The Iran conflict has added complexity here as, in theory, geopolitical stress should support the gold price. In practice, investors treated the shock as more inflationary than systemic with higher oil prices increasing inflation worries, which raised expectations for higher interest rates. In lockstep the US dollar also strengthened in the risk-off move, which reduced support for gold further.

Gold was still up 6% over the year to the end of May, but its recent behaviour has been uncomfortable for investors who expected it to protect portfolios immediately.

Figure 1: Gold price too far too fast

Despite gold’s aesthetic, psychological and symbolic character traits it should not be considered a perfect portfolio hedge. It can be thought of as "imperfect insurance". It can fall in value, be volatile, and produces no income. However, it still earns a place in a diversified portfolio if it behaves differently from equities and bonds at important points in the cycle. This is especially relevant today as bonds do not always protect portfolios when the shock is caused by inflation, energy prices or fiscal concerns. Gold may be best seen as a small alternative allocation that improves portfolio robustness, rather than as a growth asset that must keep rising.

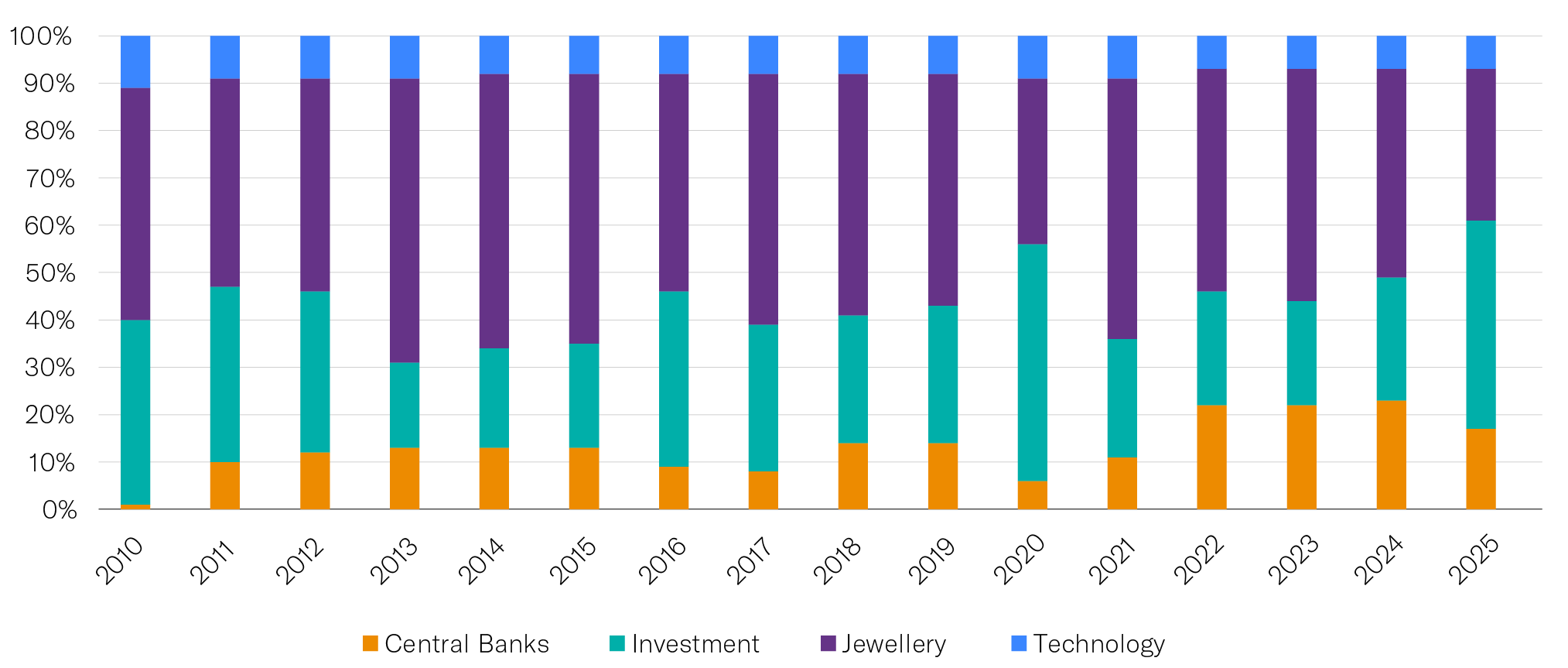

The demand picture remains broadly supportive, despite the short-term pause. Gold demand comes from four main sources: jewellery, investment, central banks and technology (figure 2). Jewellery is usually price-sensitive, so higher prices can reduce buying. Exchange Traded Funds (ETF) demand is more momentum-driven with higher prices leading to higher demand. Central banks are long term holders with their demand reflecting reserve management and diversification away from the US dollar. Gold’s industrial demand classified as “technology” for use within electronics and semiconductors is stable but proportionately small.

The short-term risk is that when gold becomes expensive, marginal buying can slow and negative momentum can weigh on prices. The long-term rationale for owning gold, namely being a store of value in times of uncertainty, having multiple sources of demand and the diversifying attributes from traditional equities and bonds remains intact.

Figure 2: Gold demand is broad

Source: https://www.ecb.europa.eu/press/other-publications/ire/html/ecb.ire202606.en.html

Sources: IMF, World Gold Council and ECB staff calculations, as at 31 December 2025

Note: “Central banks” = net purchases by central banks & international financial institutions such as the IMF or the BIS. “Investment” = purchases of gold bars, coins and ETFs. “Jewellery” = purchases for making gold jewellery. “Technology” = gold used in industrial applications.

Gold supply remains another long-term support with mine production broadly flat over the past decade, even though the gold price has risen sharply. That is because new mines take years to discover, permit, finance and extract, so higher prices doesn't create new supply quickly. Static supply does not guarantee rising prices, but it does mean that changes in demand can have a larger effect. Put differently, when more buyers want gold, the market can’t easily respond by producing much more of it.

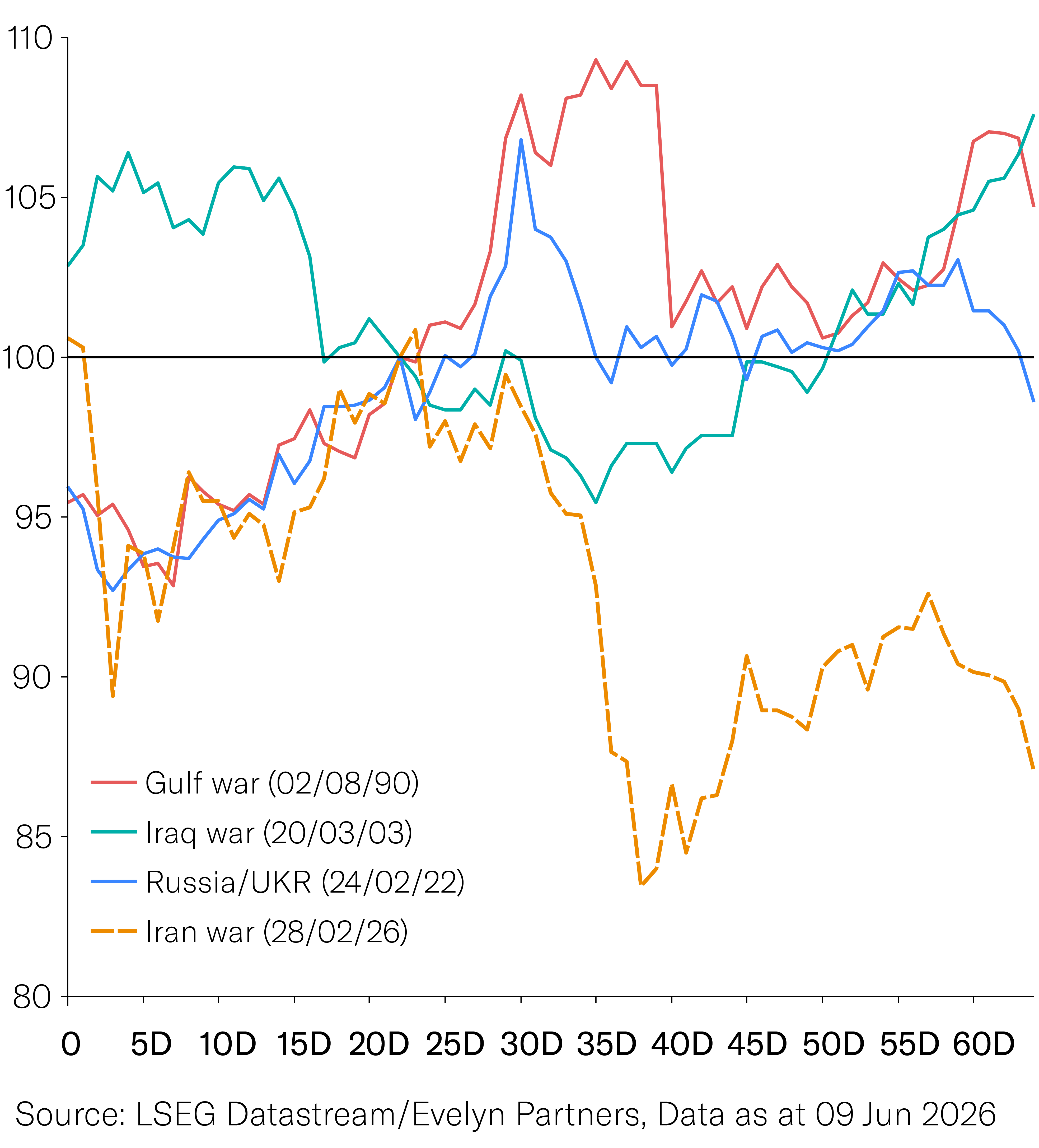

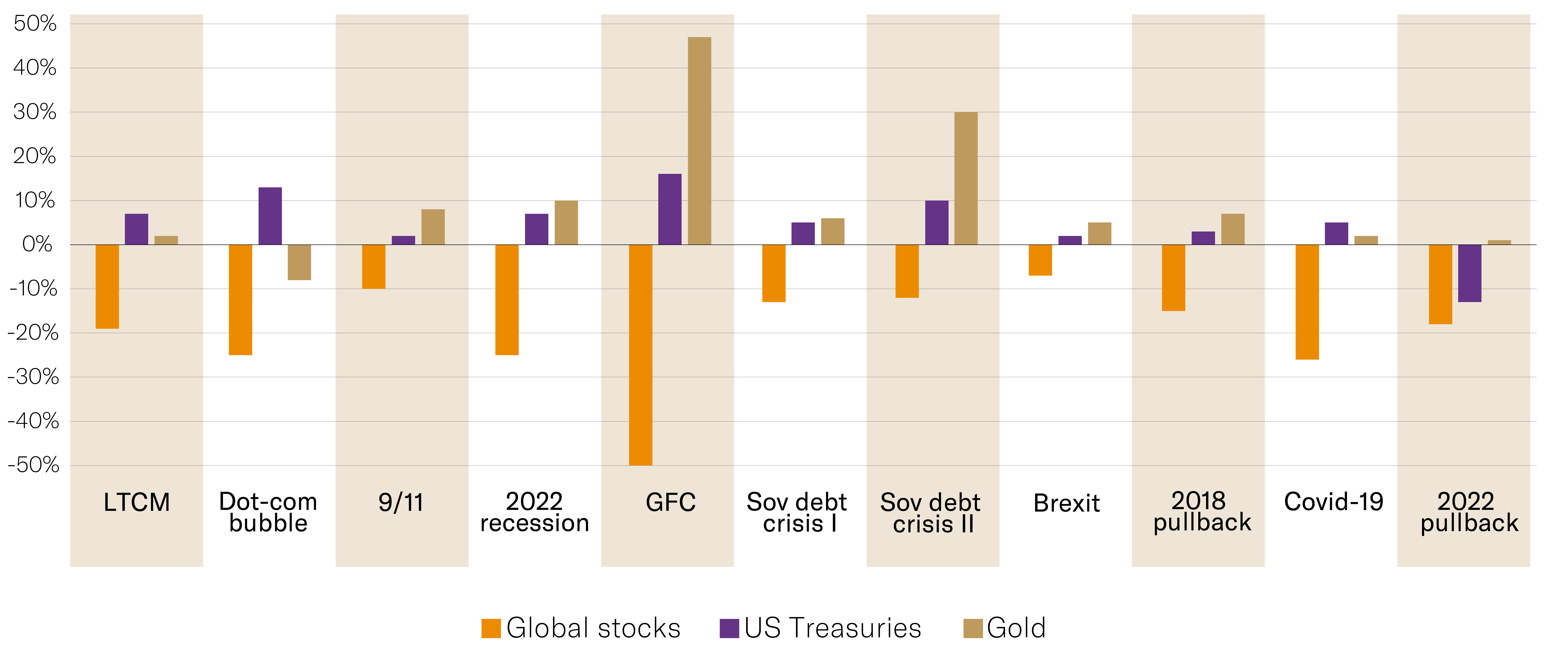

The 2026 Iran conflict has shown the limits of gold as a short-term diversifier (figure 3). During this period of market stress, gold fell alongside other diversifiers and did not provide the safe-haven performance many investors expected. This is not unusual: hedges can fail over weeks or months if other forces, such as interest rates dominate. The longer-term record is more encouraging with gold delivering stable to positive performance versus equities during different crises (figure 4). An important dynamic to be aware of here are emotional biases, gold is not intended to eliminate portfolio volatility, but to provide different sources of return when traditional assets come under pressure. Short-term discomfort should not override the long-term rationale for holding it.

Figure 3: Gold was not a short-term diversifier in the Iran conflict

Figure: 4: but its longer-term record remains helpful.

Source: Bloomberg, ICE Benchmark Administration, World Gold Council

Notes: Returns in US dollars for ‘Global stocks’: FTSE All World Index; ‘US Treasuries’: Bloomberg Barclays US Treasury Index; ‘gold’: LBMA Gold Price PM. Dates used: Black Monday: 9/1987 - 11/1987; LTCM: 8/1998; Dot-com: 3/2000 - 3/2001; September 11: 9/2001; 2002 recession: 3/2002 - 7/2002; global financial crisis (GFC): 10/2007 - 2/2009; Sovereign debt crisis I: 1/2010 - 6/2010; Sovereign debt crisis II: 2/2011 - 10/2011; Brexit: 23/6/2016 - 27/6/2016; 2018 pullback: 10/2018 - 12/2018; COVID-19: 31/1/2020 - 31/3/2020; 2022 pullback: 1/2022 – 12/2022.

Gold can also be compared with other diversifiers, not just with equities. Hedge funds can diversify but often come with complexity, higher fees and manager selection risk. Government bonds are income-producing, but they can fail as a hedge when inflation or rising yields drive the sell-off, as many investors experienced in 2022. Gold has recently performed strongly versus both hedge funds and US government bonds, leaving it vulnerable to technical reversals. That does not invalidate its role; it simply means investors should avoid chasing it after sharp rallies. A disciplined strategic allocation, rebalanced over time, is more appropriate than reacting to headlines.

Gold has not outlived its usefulness as a hedge, but investors should be clear about what type of hedge it is. It is not a perfect short-term protection tool and it should not be expected to rise during every geopolitical shock. In 2026, overstretched prices, higher interest rate expectations and slowing central bank buying have all reduced its near-term appeal. However, the long-term case remains, government debt is high, inflation uncertainty persists, supply is limited, central banks still have structural reasons to own gold and bonds may be less reliable when the problem is inflation rather than recession.

Our conviction is not to abandon gold, but to size it sensibly, treat it as portfolio insurance, and accept that insurance does not always pay out immediately. Gold still has a portfolio role, but it diversifies risk rather than guaranteeing returns.

Some of our Financial Services calls are recorded for regulatory and other purposes. Find out more about how we use your personal information in our privacy notice.

Your form has been submitted and a member of our team will get back to you as soon as possible.

Please complete this form and let us know in ‘Your Comments’ below, which areas are of primary interest. One of our experts will then call you at a convenient time.

*Your personal data will be processed by Evelyn Partners to send you emails with News Events and services in accordance with our Privacy Policy. You can unsubscribe at any time.

Your form has been successfully submitted a member of our team will get back to you as soon as possible.