It is time in the market, not timing the market

It is time in the market, not timing the market

It is time in the market, not timing the market

Before looking at why or how people try to time the markets, it is important to consider stock market volatility. This is a mathematical measure of the erratic up-and-down movements we see in share prices. Volatility is often what unnerves first-time investors who have grown used to the certainty of money in the bank.

Consider a company like Unilever. The consumer goods giant has dozens of brands from Dove to Domestos, which it makes and sells in countries across the globe from Canada to Cameroon. Its share price reflects how each of those products are selling in each of those markets, as well as investors’ best guesses for how those products will perform in the future. These factors constantly change, so its share price will naturally move up and down to reflect those changes – volatility.

One way around this volatility is to diversify – in other words, buy lots of shares. Buying any one company can be a rollercoaster ride but buying lots of them smooths out some of the ups and downs. For example, if your Netflix shares are suffering as economies open up and people leave their homes more, your Starbucks shares might be doing better as people start to socialise and drink their coffees again.

The simplest way to diversify is to buy a fund – an active fund might have 50 stocks in its portfolio, while passive ‘tracker funds’ can buy hundreds of stocks covering a whole stock market. But even if you own every company in a market, the fact remains that markets themselves are volatile, at times very volatile.

Apart from how companies themselves are doing, markets also reflect confidence in the wider economy. Economic growth, interest rates and inflation can all have an impact even at the best of times, and that’s before we get on to less predictable events like a banking crisis or a pandemic. Introducing confidence also brings in another factor, human emotion, which is both hard to predict and prone to fluctuation.

A less extreme example of timing the markets is sitting on the side lines during periods of volatility and waiting for things to improve. And with issues such as Brexit, the US/China trade war and the pandemic causing higher market volatility in recent years, many people have been doing just that.

However, those who did this missed out on some of the best ever years to be invested, like 2016 when global markets rose +29.0% or 2019 when they were up +23.4% [1]. When bad news dominates the headlines, the good news that drives profits and share prices higher is easy to miss.

Keeping your money in cash can seem wise when markets drop sharply, but it can lead to a different error. Timing the market carries the risk of missing the ‘good’ days when share prices increase significantly. And historically, many of the best periods for stock markets have occurred during periods of extreme volatility.

For instance, between May 2008 and February 2009 in the depths of the global financial crisis the MSCI World index of leading global companies dropped by -30.4%. By the end of 2009 it had bounced back +40.8%. Anybody who pulls money out in the early stages of a volatile period could miss these good days, as well as potentially locking in some losses.

Instead of trying to time the market, we believe that spending time in the market is more likely to give you good returns over the long term. Of course this means experiencing the bad days as well as the good, but history has shown that there tends to be more of the good days and over time this difference tends to mount up significantly.

For instance, the MSCI World index of leading global companies has delivered average annual returns of +11.1% since it was launched in 1969. It has been a bumpy ride at times, but we believe that successful investing requires being patient and taking a long-term view, riding out the short-term ups and downs for the chance of a much better return over longer periods of time.

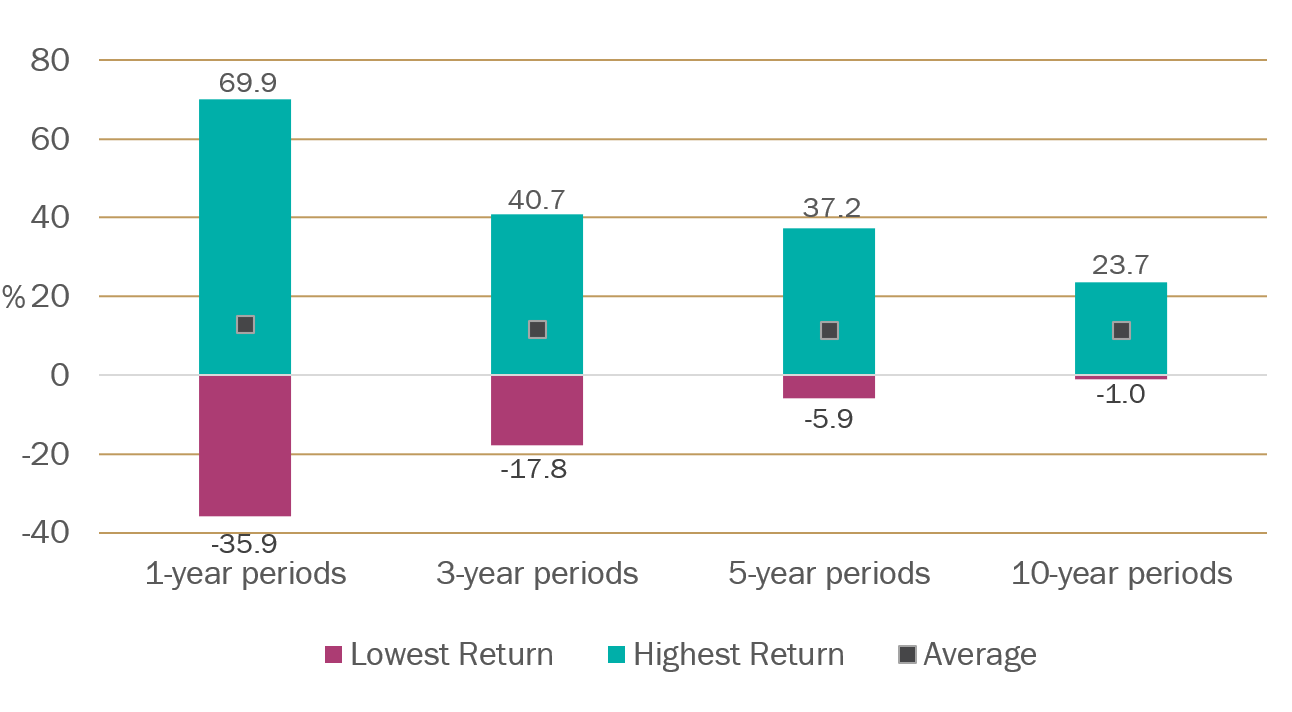

You can see evidence of this trend by looking back at how the stock market has performed in the past. We calculated the minimum and maximum annualised returns that you could have received by investing in the global stock market for every single 1, 3, 5 or 10-year period since 1970*. The results are shown in this chart.

Source: Lipper for Investment Management, as at 30 April 2022. Past performance is not a guide to future performance.

*Based on the performance of the MSCI World index from 1970 to 2022, across calendar years, with annualised returns.

The first bar shows that the returns from one-year periods (such as from 1970 to 1971) were extremely varied. Investing for one year could have given you a return between -35.9% and +69.9%. This demonstrates the volatility that can be seen in stock markets over the short term.

But over three and five-year periods this dispersion is much lower. And over ten-year periods (such as from 1970 to 1980), annualised returns ranged from -1.0% to +23.7%. Not only did the index rise in almost all ten-year periods, but the range of potential annual returns was much narrower.

Although the past can’t be taken as a reliable indicator of the future, this does suggest that investing for longer periods of time decreases the chance of overall losses. On top of this, it suggests that short-term stock market volatility tends to cancel itself out over longer periods of time, giving more consistent long-term returns.

One of the reasons that long-term investing has the potential to deliver such great returns is the power of compounding – the snowballing effect of your returns generating more returns over time. Einstein allegedly called compounding the eighth wonder of the world, and some simple examples show what he meant

Compounding is mostly achieved through dividend payments, which can be reinvested into more and more shares over time. However, you can also see its effect when companies invest their profits to grow their business – this generally results in greater profits going forward, and a higher share price. A prime example is Amazon. The company has never paid a dividend, instead reinvesting its profits into its IT systems and distribution network, turning itself into a trillion-dollar business in less than 25 years.

The power of this historical upwards trend can also be seen if you consider a fictional investor that has invested at the worst possible times over the last 40 years. If they had invested £10,000 into the global stock market at the peaks before each of the following events:

Their original £50,000 investment would today be worth £277,756** – a profit of over £225,000! Of course, past performance isn’t a reliable indicator of future performance, but it demonstrates how strongly markets have risen over the long term, even for a very unlucky investor.

**Source: Lipper for Investment Management, MSCI World Index gross of charges, as at 26 April 2022.

While steep falls in your investments can be unnerving, it’s important to bear in mind that short-term volatility is the price you must pay for the chance of higher long-term returns. Rather than try and second-guess market movements, a better strategy is to ride them out and invest for the long term. Your choice of portfolio should reflect your individual circumstances. However for those who are going to invest, the answer to the question “When is the best time?” is almost always “Now!”

If you have any questions about your investments or how Tilney can help, please contact us on 020 7189 2400 or book a free consultation to speak to one of our advisers.

[1] Lipper for Investment Management, 2016 – 2019.

[2] Morningstar

This article was previously published on Tilney prior to the launch of Evelyn Partners.

Some of our Financial Services calls are recorded for regulatory and other purposes. Find out more about how we use your personal information in our privacy notice.

Your form has been submitted and a member of our team will get back to you as soon as possible.

Please complete this form and let us know in ‘Your Comments’ below, which areas are of primary interest. One of our experts will then call you at a convenient time.

*Your personal data will be processed by Evelyn Partners to send you emails with News Events and services in accordance with our Privacy Policy. You can unsubscribe at any time.

Your form has been successfully submitted a member of our team will get back to you as soon as possible.