Artificial intelligence: from capex buildout to productivity gains

AI is driving a surge in investment, but its long-term economic impact will depend on whether adoption translates into meaningful productivity gains.

AI is driving a surge in investment, but its long-term economic impact will depend on whether adoption translates into meaningful productivity gains.

Since the launch of ChatGPT in late 2022, artificial intelligence (AI) has become one of the dominant themes in financial markets. Investment in data centres, computing infrastructure and power capacity has accelerated rapidly and a number of companies in the supply chain have delivered exceptional earnings growth.

For investors, the challenge is separating the excitement surrounding AI from the tangible benefits it may ultimately deliver.

Investors have not waited for definitive proof that AI will transform the wider economy.

Market leadership has become increasingly concentrated among a small group of technology companies, often referred to as hyperscalers. These companies are investing heavily in the infrastructure required to develop and deploy AI, and their profits have increasingly diverged from the broader market. The scale of this divergence shows how much growth is already being priced in.

Figure 1: Hyperscaler profitability versus broader market

Much of the market’s enthusiasm reflects a growing belief that AI could become a general-purpose technology - a technology with applications across large parts of the economy.

Previous examples include electricity, railways, and the internet. Each transformed the way businesses operated, created new industries and ultimately contributed to stronger productivity growth.

Figure 2: Historical productivity gains from general-purpose technologies

The lesson from history is that this process takes time. Large amounts of capital are often invested upfront, while productivity gains emerge only later as businesses adapt processes, develop new applications, and reorganise how they operate.

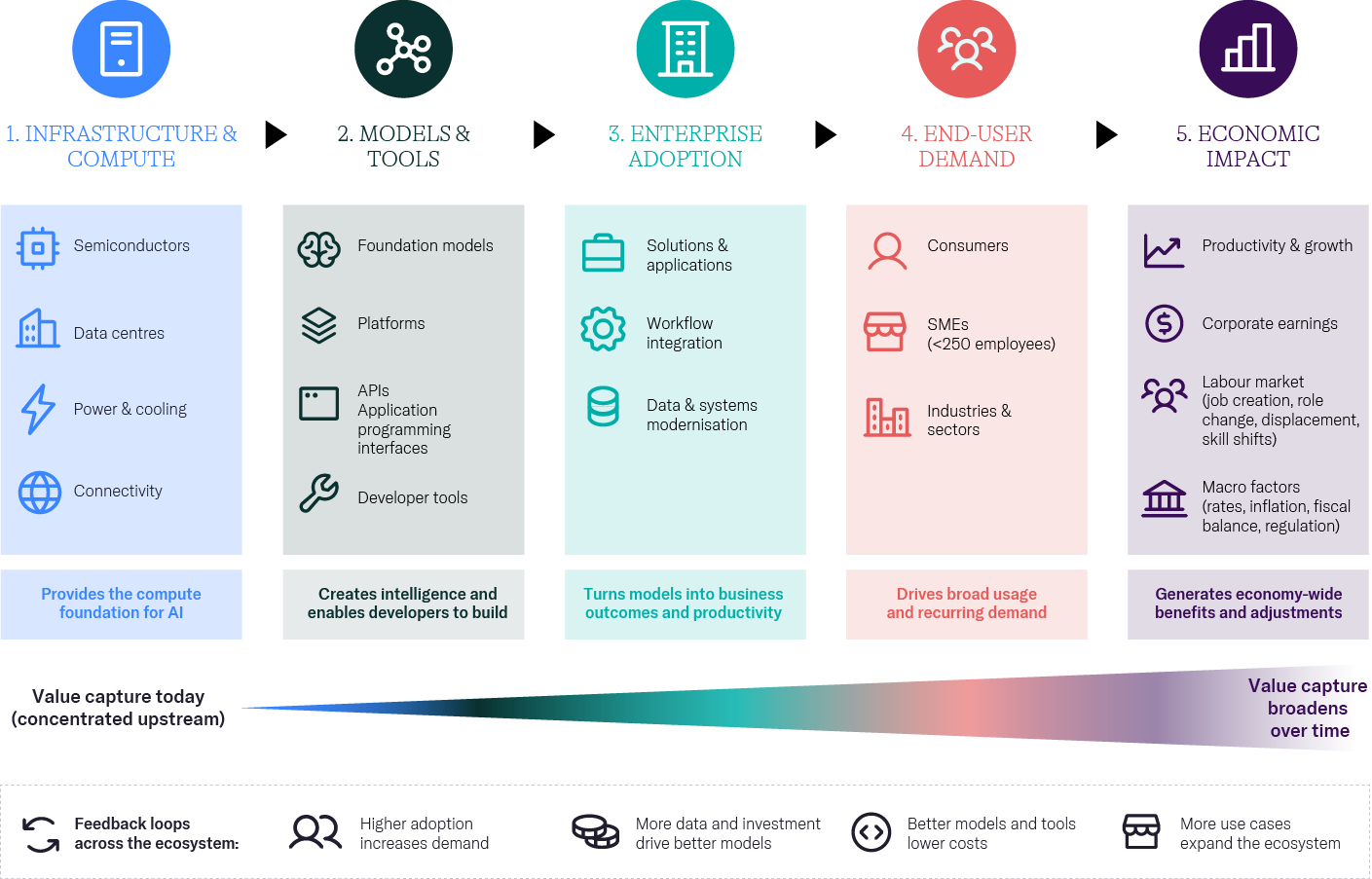

While much of the public discussion focuses on tools such as ChatGPT, these applications represent only one part of a broader ecosystem.

The AI value chain begins with the infrastructure required to train and run AI models, including semiconductors, data centres and power infrastructure. From there, value flows through AI models and software applications before reaching businesses, consumers and, ultimately, the wider economy.

The companies building AI may not ultimately be the same companies that derive the greatest economic benefit from using it.

Figure 3: The AI ecosystem

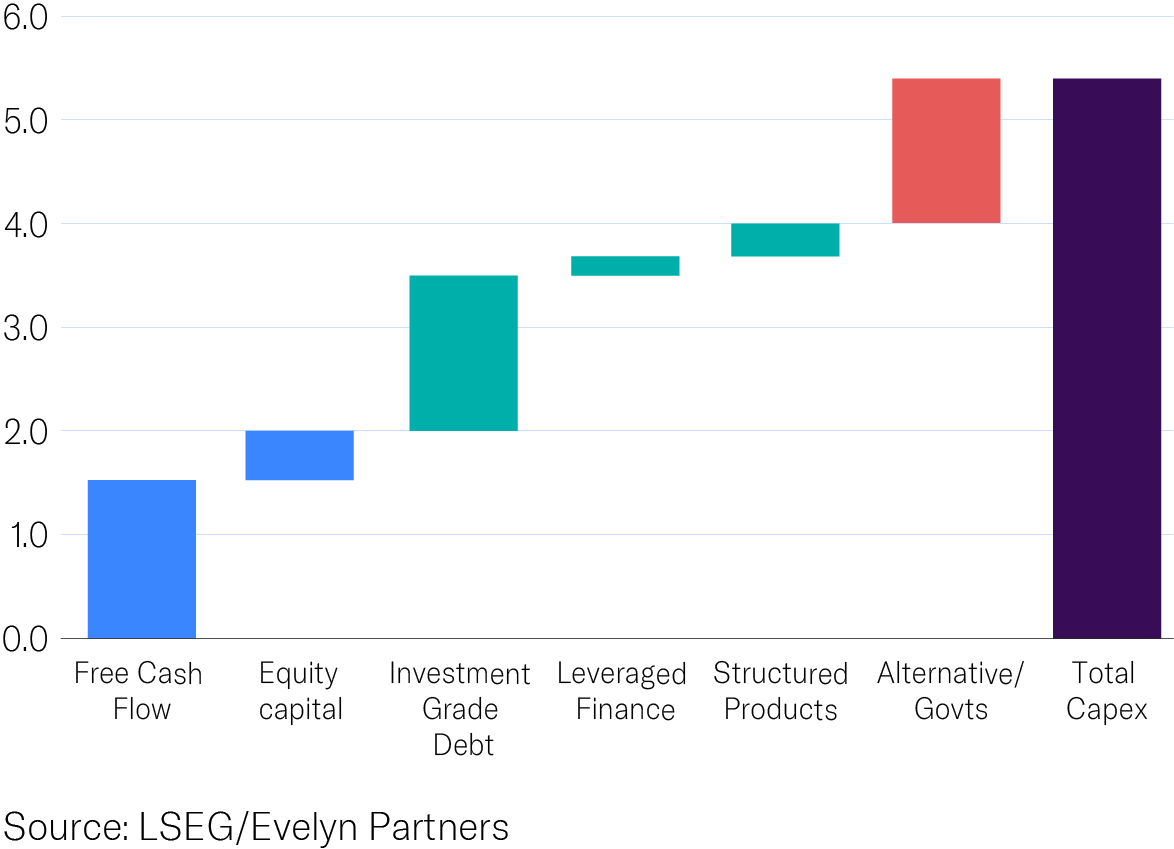

The scale of the AI buildout is substantial. McKinsey estimates that AI-related data centre investment alone could reach $7 trillion in aggregate by 20301, with AI processing loads accounting for most of the demand. Much of the investment to date has been funded by the strong cash flows and balance sheets of large technology companies. However, as infrastructure requirements continue to expand, a wider range of funding sources is likely to be required.

AI Capex Funding Sources ($tns)

While investment-grade debt markets can support much of the near-term buildout, a wider range of public and private capital is likely to be required over time.

This is increasingly drawing in infrastructure investors, private capital providers, and credit markets. Data centres and energy infrastructure are emerging as important beneficiaries of the AI buildout.

As a result, the AI investment story extends beyond listed technology companies and into a broader range of asset classes.

Among the most visible consequences of the AI buildout is the rising demand for electricity. Data centres already account for around 4–5% of US electricity consumption, with that figure expected to rise to 9% or more by 20302 as AI adoption increases.

This creates both opportunities and constraints. Rising demand supports investment in power generation, transmission networks and energy infrastructure, while grid capacity and power availability are becoming important constraints on future expansion.

At the same time, the energy mix is evolving. Renewables are becoming increasingly cost competitive and are expected to supply a growing share of future electricity demand, helping support the next phase of the AI buildout.

For investors, power is emerging as both a potential bottleneck and a source of opportunity.

The key question is whether today's infrastructure investment ultimately translates into meaningful productivity gains.

To frame the possible paths ahead, we consider three broad scenarios for how AI could affect the economy through 2030.

At present, the evidence appears most consistent with (2) gradual adoption. AI capabilities continue to improve rapidly, but widespread productivity gains are likely to emerge more gradually as businesses adapt processes, invest in systems and identify practical applications.

The longer-term investment implications of AI remain uncertain, but several observations can be made:

The infrastructure buildout remains the clearest near-term opportunity

The current phase of the AI cycle continues to be driven by investment in computing power, data centres, electrification, and supporting infrastructure.

Productivity gains are the next test

The long-term investment case depends on whether businesses can translate AI capabilities into higher productivity, margins and earnings growth.

Diversification matters more as concentration rises

A small number of companies have accounted for an increasing share of market returns.

Opportunities extend beyond public equities

The AI buildout is creating demand for infrastructure, real assets and private capital, making the theme relevant across a broader range of asset classes.

Market leadership is likely to broaden

Much of the early benefit has accrued to a small number of companies in the AI supply chain. Over time, opportunities may increasingly emerge among businesses adopting AI rather than simply building the required infrastructure.

Maintaining exposure across asset classes, sectors, and regions remains one of the most effective ways to navigate the opportunities and risks created by AI.

For investors, the challenge is shifting from identifying whether AI matters to understanding where future benefits may emerge and whether those benefits are already reflected in market prices.

As with previous technological revolutions, the path from investment to productivity is unlikely to be linear. While AI has the potential to reshape parts of the economy over the coming decade, the winners and losers may look very different from those driving markets today.

The Cost of Compute: A $7 Trillion Race to Scale Data Centers, McKinsey, 29 May 2025.

Powering Intelligence: Analyzing Artificial Intelligence and Data Center Energy Consumption, EPRI, 2024

Some of our Financial Services calls are recorded for regulatory and other purposes. Find out more about how we use your personal information in our privacy notice.

Your form has been submitted and a member of our team will get back to you as soon as possible.

Please complete this form and let us know in ‘Your Comments’ below, which areas are of primary interest. One of our experts will then call you at a convenient time.

*Your personal data will be processed by Evelyn Partners to send you emails with News Events and services in accordance with our Privacy Policy. You can unsubscribe at any time.

Your form has been successfully submitted a member of our team will get back to you as soon as possible.