How diversified is your portfolio?

As we enter the ninth year of a bull market, the second longest in history, ensuring portfolios are diversified is important.

As we enter the ninth year of a bull market, the second longest in history, ensuring portfolios are diversified is important.

Following the last global financial crisis and during periods of market stresses, we have already witnessed correlations, or co-movement amongst asset classes trending together. This has raised doubts over the traditional approach to asset allocation, and the diversification benefits achieved across equities and bonds in particular.

The traditional approach to asset allocation comprised of a fixed allocation to equities and bonds, but now also includes alternatives, such as real estate, private equity and commodities which are held over the medium to long term. Equities and bonds have recently shown a relatively low correlation, with investors preferring the lower, but safer returns of bonds, particularly during times of flight-to-quality.

History, however, shows the relationship between stocks and bonds to be more dynamic, switching through prolonged periods of positive and negative correlation. It can also be demonstrated the relationship between stocks and bonds has been strongly influenced by a number of macroeconomic factors. This suggests traditional models used to balance portfolio risk and return using different asset classes may be misleading, particularly as they are often divorced from changes in macroeconomic indicators.

To better understand the relationship between asset classes and what drives their risk/return characteristics we first need to identify their building blocks. For example, the returns on equities will be influenced by a number of risk factors, including volatility, size, economic growth and inflation, to name just a few. The returns on bonds will be shaped by a number of risk exposures such as interest rates and the risk of default.

Though there are an infinite number of risks influencing returns on each asset class, there are four key macroeconomic factors that are common across all; interest rates, inflation, economic growth and unemployment. The difficulty for investors is how to invest directly into each of these macroeconomic factors using asset classes. Some exposures, such as inflation risks, can be reduced through the use of inflation-linked bonds, but accessing economic growth through equities has often been considered a loose proxy. Another issue is how much to allocate to each of these individual economic risks in a portfolio, which will often require frequent changes. It is these practical challenges that may have prevented the widespread adoption of a risk-based approach when constructing portfolios.

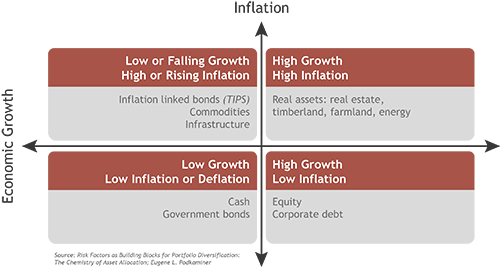

An alternative approach could be to analyse the behaviour of equities, bonds and alternatives under various economic scenarios. By understanding how asset classes respond under diverse economic conditions we can identify the relationships between them and how they will react to changes in the macroeconomic environment. For instance, periods of high growth and low inflation would favour a higher weighting to equities and corporate bonds. On the other hand, times of falling growth and rising inflation would benefit inflation-linked bonds, commodities and infrastructure.

The table below highlights different macroeconomic scenarios and the groups of asset classes expected to benefit under such conditions.

Here, you could construct a portfolio according to your economic outlook and the current stage in the business cycle and tactically shift the allocations to asset classes likely to benefit. This should produce a diversified but dynamic portfolio cognisant of changes in economic conditions.

What is important to note here is the longer current market conditions continue, the more conscious we are of a large and abrupt shift in such conditions and the need to identity the trigger(s) for this. For example, could it be inflation rising more than expected with concerns over an overheating US economy? Understanding a portfolio’s underlying exposure to various risks or outcomes can therefore not only help reduce your exposure to large losses during market falls, but also aid your understanding of the changing relationships across asset classes.

In summary, we can see how a risk-based approach incorporating macroeconomic risks can be integrated with a traditional asset allocation to enhance a portfolio’s profile. Theoretically, this should result in identifying lower correlations across asset classes, leading to an optimal construction of a portfolio in terms of risk and return.

Whilst this approach can help improve the understanding of the underlying risks in a portfolio and relationships across different asset classes, it is always important to remember that fundamental valuations will play a pivotal role in portfolio management. The past decade has seen valuations on both bonds and equities reaching record levels. Here, any sudden and abrupt change in market conditions could see both asset classes underperforming, irrespective of the underlying economic environment. It is therefore crucial not to forget the importance of market valuations in your investment decision making.

The value of investments and the income from them can fall as well as rise and the investor may not receive back the original amount invested.

DISCLAIMER

By necessity, this briefing can only provide a short overview and it is essential to seek professional advice before applying the contents of this article. This briefing does not constitute advice nor a recommendation relating to the acquisition or disposal of investments. No responsibility can be taken for any loss arising from action taken or refrained from on the basis of this publication. Details correct at time of writing.

This article was previously published prior to the launch of Evelyn Partners.

Some of our Financial Services calls are recorded for regulatory and other purposes. Find out more about how we use your personal information in our privacy notice.

Your form has been submitted and a member of our team will get back to you as soon as possible.

Please complete this form and let us know in ‘Your Comments’ below, which areas are of primary interest. One of our experts will then call you at a convenient time.

*Your personal data will be processed by Evelyn Partners to send you emails with News Events and services in accordance with our Privacy Policy. You can unsubscribe at any time.

Your form has been successfully submitted a member of our team will get back to you as soon as possible.