In this case study, we walk through a client example of what end of tax year planning Alexander and Lucy should be considering, including: pensions contributions, ISA allowances, personal allowances, tax reliefs, charitable gifts and gift allowances.

Alexander (52) is married to Lucy (50), they have two children, Henry (16) and Emily (13). Alexander is an Architect and has been a partner in the same firm for the last ten years. His earnings will be £325,000 in 20/21 and have been a similar level for the last few years.

Lucy has been made redundant from her long term position just before Christmas. Her annual salary was £50,000 and due to her length of service, she will be receiving a redundancy package of £113,000 of which £30,000 is tax free, taking her taxable earnings for 20/21 to £124,000.

Lucy is a deferred member of the defined benefit scheme, which closed several years ago. Since then she has been contributing to her Group Personal Pension scheme at £11,000 per year via salary sacrifice.

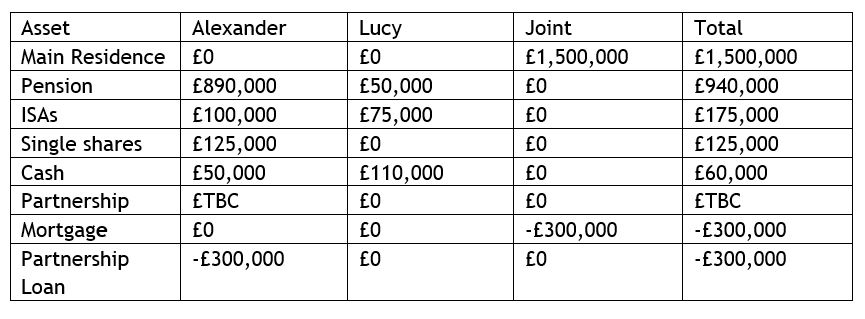

Assets

Lucy’s cash balance includes cash from her redundancy payment.

Objectives

- Building funds for the future

- Should they pay some of the mortgage off?

- Minimising tax exposure

- What to do with the redundancy payment?

Considerations for end of year tax planning

Alexander could make a pension contribution of £34,000 gross. Alexander is impacted by the tapered annual allowance. His annual allowance in 2020/21 is £4,000. He could carry forward £10,000 annual allowance from each of the previous three tax years. He would need to write a cheque for £27,200 and then claim the remaining tax relief of £8,500 through his tax return. Money within a pension environment is not accessible until Alexander reaches 55. At retirement 25% of the fund is available tax free and the remainder is subject to income tax at the applicable rate.

Another option might be to consider applying to protect his lifetime allowance. The lifetime allowance is the amount that you are allowed within all pension funds without incurring an additional lifetime allowance charge. The current level is £1,073,100. As Alexander has made no pension contributions since February 2016, he can apply for Fixed Protection 2016 and increase his Lifetime Allowance to £1,250,000.

The Lifetime Allowance increases by CPI each year, assuming an increase of 2% per year, the standard lifetime allowance would surpass £1,250,000 in 2028. 5% annual growth on his pension funds would see him breach the LTA in 2026. Alexander needs to weigh up tax relief now, versus managing for lifetime allowance later.

Lucy can make a pension contribution of up to £116,000 gross. For the last four years she has contributions of £11,000 per year into her pension, meaning she had £29,000 to carry forward from each of the previous three tax years and the current one. She would need to write a cheque of £92,800. In the end Lucy decides to make a pension contribution of £75,000 gross. The immediate cost is £60,000. This takes her out of higher rate tax and also restores her personal allowance

Both decide to add the maximum contribution of £20,000 to their Stocks and Shares ISA for 20/21. An ISA provides a tax efficient environment in which investment assets can grow, being free from income tax and capital gains tax.

Another option for Alexander is to consider investing in a Venture Capital Trust (VCT), Enterprise Investment Scheme (EIS), or Seed Enterprise Investment Scheme (SEIS). As his ability to add funds to a pension is so limited, this allows him another route to investments offering tax relief. He will need to risk appetite and the time scale that goes along with these investments. VCTs and EISs attract 30% income tax relief, while SEIS attracts 50%, subject to investment limits VCTs, EIS and SEIS are high risk investments which are only suited to certain investor profiles = see briefing notes for a full explanation of the risks involved.

In addition they could consider whether or not to crystallise gains on Alexanders shares to use his CGT allowance, or transfer some shares to Lucy so that the dividend are taxed at her marginal rates.

The mortgage is on a fixed rate and paying this off would attract a penalty. In addition, as the rate is very low, it is decided contributions to pensions will give them a better return in the long run.

The children can contribute £9,000 to Junior ISAs; a slight quirk in the ISA allowance rules means Henry can also take out a cash ISA of £20,000. In addition, both children could have pensions funded with a contribution of £3,600 gross, £2880 net.

Please note this case study is for illustration purposes only and you are strongly advised to seek professional advice before making financial decisions.

Read our article - The Annual Allowance - pension contributions 2020/21 Listen to our podcast: Financial Planning for tax year end

DISCLAIMER

By necessity, this briefing can only provide a short overview and it is essential to seek professional advice before applying the contents of this article. This briefing does not constitute advice nor a recommendation relating to the acquisition or disposal of investments. No responsibility can be taken for any loss arising from action taken or refrained from on the basis of this publication. Details correct at time of writing.

Risk warning

Investment does involve risk. The value of investments and the income from them can go down as well as up. The investor may not receive back, in total, the original amount invested. Past performance is not a guide to future performance. Rates of tax are those prevailing at the time and are subject to change without notice. Clients should always seek appropriate advice from their financial adviser before committing funds for investment. When investments are made in overseas securities, movements in exchange rates may have an effect on the value of that investment. The effect may be favourable or unfavourable.

Source: HMRC 2020/21.

Ref: 25321lw