After setting up its specialist unit to investigate, HMRC has now relieved itself of current concerns it had about Family Investment Companies (FICs). FICs of all kinds, and especially those holding property, have weathered the storm of recent and proposed tax changes and remain a tax efficient option for many investors.

Low rates of tax for companies compared to the higher personal tax rates means that owning property through a company can be tax-efficient. However, with corporation tax rises looming, property owners are asking if this continues to be the case.

The answer is ‘yes’! From 1 April 2023, corporation tax is rising to 25% from 19% for family or “closely-held” investment companies, irrespective of their profit levels. For other company types the higher rate only applies when profits reach £250,000. This is still a low rate compared to the 45% additional rate of personal tax and note that dividend income received by investment companies is still non-taxable for the most part. Better still is that FICs that own property portfolios have been specifically exempted from the automatic tax rate rise and so will continue to pay 19% corporation tax, provided that the annual profits of the property FIC are less than £250,000.

Other tax advantages of the company structure remain; for example, companies can claim loan interest in full as an expense (there can be restrictions where the interest exceeds £2 million), whereas individuals may not.

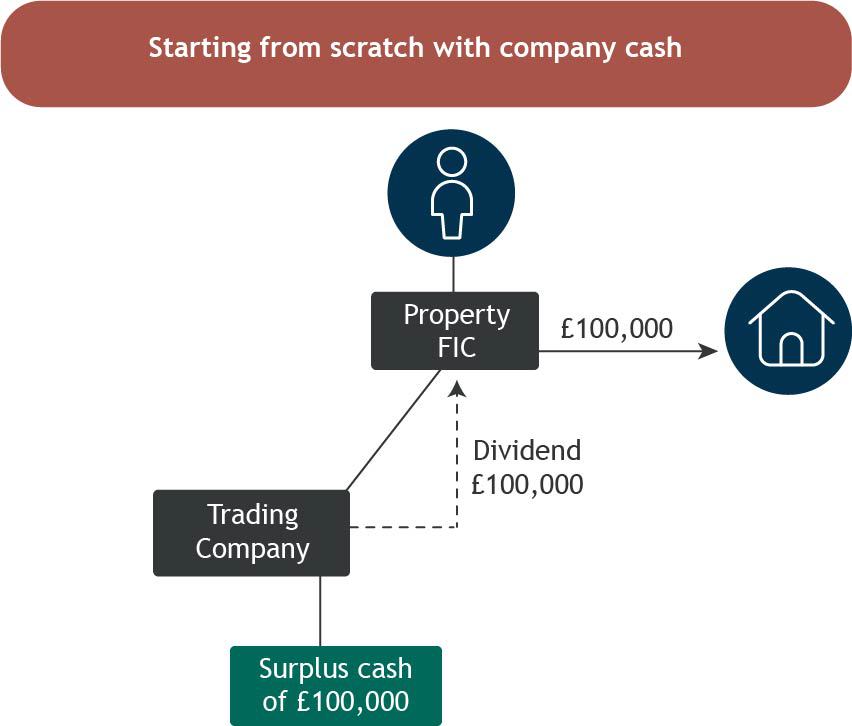

Starting from scratch with company cash

Julia Rosenbloom, Partner, Private Client Tax Services says: ‘I frequently work with business owners whose companies are making profits in excess of what they need to fund their personal lifestyles. Where cash is not required for the main business of the company, people will naturally want to invest that money so it works for them.

If the company pays it to the business owner as a dividend it will be charged to income tax at a rate of up to 38.1% (39.35%. from April 2022). So, taking £100,000 could leave just £61,900 to put towards a new property (£60,650 from April 2022).

Instead of taking the cash out as a dividend, it’s possible to redirect the cash to a FIC, without suffering tax in the process.’

What about starting from scratch with personal cash?

One structure to consider is a commercial loan of cash to a company. The company makes its investments, generates rental income and pays a relatively low tax rate on rental profits. An individual who wants to access the rental income, can draw down the loan tax-free. For many, this means getting rental income at a 19% effective tax rate, rather than 45% for additional rate taxpayers. Once the loan has been repaid by the company, the individual will have to pay income tax on dividends when they withdraw the rental income.

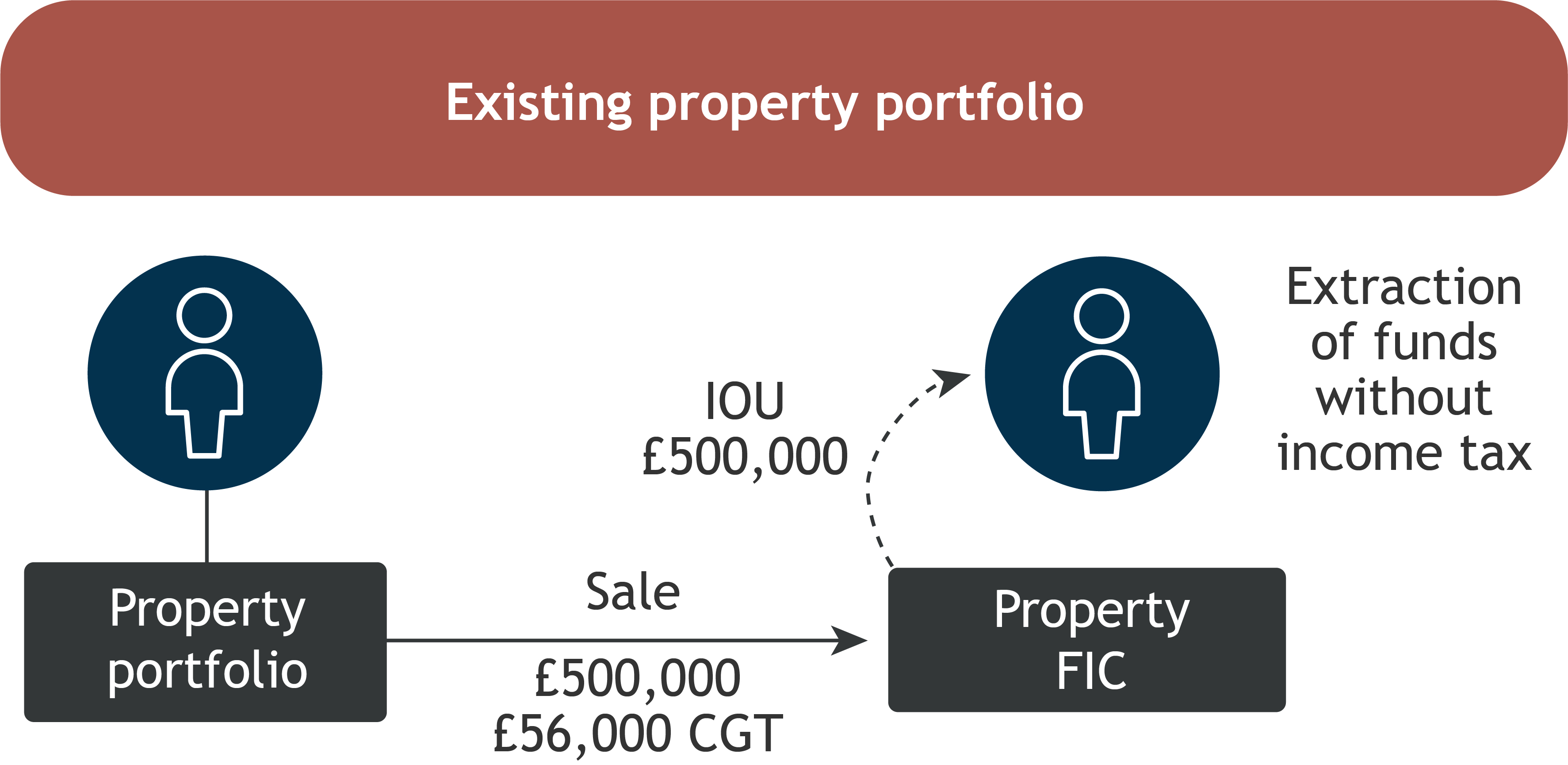

Existing property portfolios

Individuals who want to move property into a company should consider the capital gains tax (CGT) consequences: a transfer of property into a company is deemed to be a sale for CGT purposes, even if no cash changes hands.

In some cases, incorporation relief may apply to prevent any CGT charge on such a ‘deemed sale’, whilst at the same time increasing the base cost of the properties in the company to current market value. This ‘double advantage’ could mean significantly less tax is paid on a subsequent disposal by the company.

An alternative to this would be actually to sell the properties into the FIC to bank the current low rates of CGT (20% and 28%) to hedge against the risk of CGT rates increasing in the future (there has been speculation that CGT rates could eventually be aligned with income tax rates.)

For example, an individual who sells property worth £500,000 with inherent gains of £200,000, could pay up to £56,000 in CGT (and some stamp taxes). The individual can then draw out the rental income from the FIC up to an amount of £500,000 without incurring personal tax. So, a £56,000 CGT liability replaces future income tax liabilities of up to £196,750. Once the loan has been repaid, there would be an income tax charge upon extracting the rent from the FIC.

And in the case of inheritance tax (IHT), holding property in a company affords a wider range of succession options which can then reduce IHT exposure. This is good, as property investments do not benefit from any form of IHT relief.

Conclusion

Whilst tax rules can change, which may create inefficiencies in the future, for the majority of property investors, the advantages of holding property investments via FICs continue to stand out and these advantages could be significant. Provided they make sense for tax and other purposes, they should be given serious consideration.

If you would like to talk to us about the management of your property portfolio or the benefits of a FIC, please get in touch.

View our insights guide - Covid, Brexit and tax: the impact on real estate funds View our real estate page

DISCLAIMER

By necessity, this briefing can only provide a short overview and it is essential to seek professional advice before applying the contents of this article. This briefing does not constitute advice nor a recommendation relating to the acquisition or disposal of investments. While considerable care was taken to ensure the information contained within this article was accurate and up to date at the time of publication, no warranty is given as to the accuracy or completeness of the information. No liability is accepted for any errors or omissions in such information, or any action or inaction taken on the basis of this publication.

Please remember investment involves risk. The value of investments and the income from them can fall as well as rise and investors may not receive back the original amount invested. Past performance is not a guide to future performance.

Evelyn Partners Investment Management LLP

Authorised and regulated by the Financial Conduct Authority.

Registered in England No. OC 369632. FRN: 580531

Evelyn Partners Investment Management LLP is part of the Evelyn Partners group.

© Evelyn Partners Group Limited 2022

Ref: NTNPW1121107