UK Carbon Border Adjustment Mechanism to be implemented by 2027

On 18 December 2023, the Government published the summary of responses to the consultation on addressing carbon leakage risk to support decarbonisation.

One of the measures included in the consultation was a UK Carbon Border Adjustment Mechanism (UK CBAM). The Government has confirmed that it will implement a UK CBAM by 2027.

What are Carbon Border Adjustment Mechanisms?

Carbon Border Adjustment Mechanisms (CBAMs) apply a carbon price to selected imported goods so that they are subject to the same carbon price as locally produced goods. The EU implemented the world’s first CBAM from 1 October 2023. It is currently in a transitional phase, with importers of goods covered by the scheme having to report the amount of goods imported and their embedded carbon emissions on a quarterly basis. The first reports for the period 1 October 2023 to 31 December 2023 are due to be filed by 31 January 2024.

Who is liable for CBAM?

Under the existing EU CBAM, and the proposed UK CBAM, importers of imported goods within the scope of the CBAM are liable on the basis of emissions embedded in the imported goods.

How is CBAM liability met?

The EU CBAM is currently in a transitional phase, meaning that there is no liability, but reporting is required. When the full CBAM comes into force on 1 January 2026, importers will need to declare the quantity of imported goods and their embedded emissions annually and surrender CBAM certificates to cover the emissions. The price of certificates will be based on the price of EU Emissions Trading Scheme (EU ETS) allowances.

The proposed UK CBAM will not involve the purchase or trading of certificates. Further details on the design and delivery of UK CBAM will be subject to consultation in 2024.

Which sectors are covered by CBAM?

The proposed UK CBAM has a slightly different scope to the EU CBAM. The sectors covered are:

Sector | EU | UK |

Aluminium | Yes | Yes |

Cement | Yes | Yes |

Ceramics | No | Yes |

Fertiliser | Yes | Yes |

Glass | No | Yes |

Hydrogen | Yes | Yes |

Iron and steel | Yes | Yes |

Electricity | Yes | No |

The UK notably proposes to include ceramics and glass, which are not covered by the EU CBAM, and excludes electricity which is covered by EU CBAM.

Excluding electricity seems to have been on the basis that there is a low risk of carbon leakage occurring given that most imported electricity comes from the EU where it is already subject to a comparable carbon price. Subjecting it to the UK CBAM would have added administrative burden with no real carbon leakage risk to be tackled.

The precise list of products which are to be within the scope of UK CBAM will be the subject of further consultation in 2024.

Which emissions are included within UK CBAM?

The UK CBAM will apply to embedded Scope 1, Scope 2 and select precursor product emissions in imported products so that the coverage is comparable with the UK Emissions Trading Scheme (UK ETS), and imported products are subject to the same carbon pricing as domestically produced products.

Scope 1 emissions are related to direct activities of producing the product, for example as part of the manufacturing process or from burning fuel on site.

Scope 2 emissions are indirect emissions related to the use of bought electricity, heat, steam and cooling used by the manufacturer.

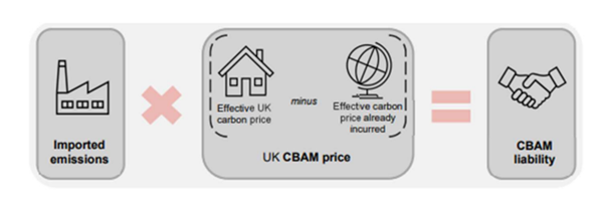

What carbon price will apply?

The UK CBAM will apply an effective carbon price to imports which matches that domestic producers are subject to. This will be based on the UK ETS price but take account of free allowances UK producers receive and other support mechanisms.

Local carbon prices paid by overseas producers will also be considered in calculating the individual charge for an import. The 2024 consultations which will follow will include detail on the criteria for recognition of carbon prices in other territories.

The CBAM liability will be calculated by multiplying the carbon price difference by the amount of emissions embedded in the affected imported products.

How does UK CBAM interact with UK ETS?

One of the tools currently used to mitigate carbon leakage risk is to give free UK ETS allowances to manufacturers in sectors at risk from international competition. With the introduction of a UK CBAM, the products within the scope of the UK CBAM would no longer be at risk from imports from territories with low carbon prices because the UK CBAM pricing for imports should put them on the same effective carbon price as a UK producer.

In July this year it was announced that the number of UK ETS allowances that can be purchased from the Government will reduce by 45% between 2023 and 2027, to contribute towards the UK’s net zero ambition.

It has been confirmed that free allocations of UK ETS allowances will be kept at current levels for industrial sectors until 2026.

A consultation was launched on 18 December 2023 for Review of Free Allocation, which explores the way in which free allocations should be targeted for industries most at risk of carbon leakage. One of the options suggested in the consultation is the phasing out of free allocations for sectors in the scope of UK CBAM. This would mirror the approach the EU is adopting, with free allowances being phased out between 2026 and 2030 for some sectors.

How can we help?

We can help with understanding your exposure to EU CBAM or UK CBAM, preparing your quarterly reports for EU CBAM, and responding to consultations.

If you have any questions or want to understand how CBAM affects your business, please contact our expert Jayne Harrold.

Source

[1] Source: Factsheet: UK Carbon Border Adjustment Mechanism

Approval code: NTEH7012467

By necessity, this briefing can only provide a short overview and it is essential to seek professional advice before applying the contents of this article. This briefing does not constitute advice nor a recommendation relating to the acquisition or disposal of investments. No responsibility can be taken for any loss arising from action taken or refrained from on the basis of this publication.

Tax legislation

Tax legislation is that prevailing at the time, is subject to change without notice and depends on individual circumstances. You should always seek appropriate tax advice before making decisions. HMRC Tax Year 2023/24.