UK SOX: how prepared are you?

Understanding the practical implications of UK SOX and preparing for a timely and smooth implementation is important. Smith & Williamson can help.

How to prepare for UK SOX

Calls for corporate governance reform have emerged from a variety of sources over the past few years. Most notably in March 2021, BEIS published its consultation paper ‘Restoring trust in audit and corporate governance’ which addresses almost all of the recommendations drawn from the independent reports of Sir John Kingman, Sir Donald Brydon and the CMA. The paper sets out measures to improve the quality of corporate governance, corporate reporting, and internal controls. The top proposed output of the paper is the implementation of a ‘UK Version of Sarbanes Oxley’. The results of the consultation indicate that any future legislation would initially focus on premium listed companies with other Public Interest Entities (PIEs) following.

At Smith & Williamson we think it is important for companies to be aware of future practical implications and how we can best serve them to prepare for a timely and smooth future implementation.

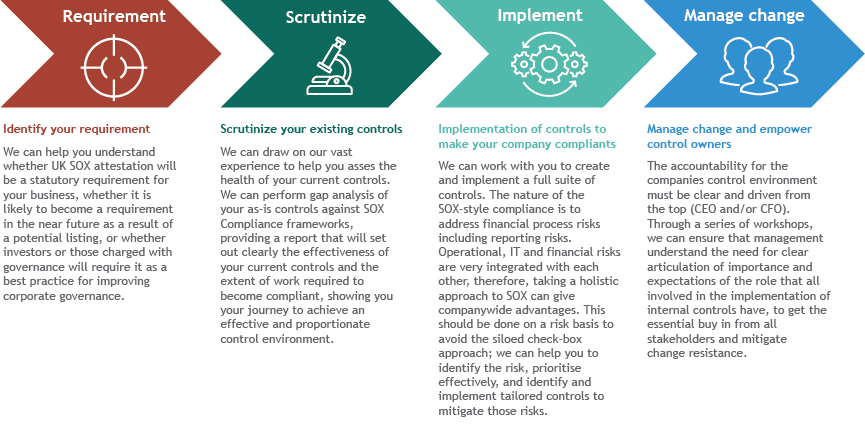

How we can help with UK SOX preparation

We are committed to journeying with our clients in their SOX readiness process from the planning stage right through to first attestation. Outlined below are some of our key plays on how to help you successfully prepare.

Frequently asked questions

When will the UK SOX requirements come into force?

While the whitepaper does not include timeframes, typically companies have two reporting years until they are required to be SOX compliant after the legislation is finalised. Thus, if the legislation is going to be finalised in 2022, we could expect to see a requirement for premium listed entities in 2024. It, most likely, will then become a requirement for UK PIEs two years later.

What are the consequences of UK SOX for directors?

Within the 3LOD model, where does the responsibility sit?

Under US SOX, it typically is in the first line of defence, however a good second line function (where it exists) should also guild and support to ensure successful implementation. So, it would be reasonable to assume that it will be the case in the UK.

For help with SOX please get in touch with:

Amanda Smith, Director, Risk Advisory

Amanda.smith@smithandwilliamson.com

Louise Roberts, Senior Manager, Risk Advisory

louise.roberts1@smithandwilliamson.com

Dilpreet Johal, Senior Manager-Technology, Risk Advisory

dilpreet.johal@smithandwilliamson.com

Smith & Williamson LLP

Regulated by the Institute of Chartered Accountants in England and Wales for a range of investment business activities.

Smith & Williamson LLP is a member of Nexia International, a leading, global network of independent accounting and consulting firms. Please see https://nexia.com/member-firm-disclaimer/ for further details.

Smith & Williamson LLP is part of the Tilney Smith & Williamson group.

Registered in England No. OC 369631.

Ref: 22037799

Disclaimer

This article was previously published on Smith & Williamson prior to the launch of Evelyn Partners.