Chief Investment Officer Chris Godding reviews the themes likely to dominate investment strategy for the remainder of the year

Speaking at a briefing in London this week, Chris Godding, chief investment officer of wealth management group Tilney which oversees £23 billion of assets, said he is expecting a period of more muted returns from equity markets through the second half of 2017 after a brisk start to the year which saw key equity markets deliver total returns of 4 – 14% in Sterling terms*. Godding cited the impact of a fading credit impulse from China and a coordinated shift in rhetoric from central banks as an inflection point that means the era of monetary policy actively driving assets prices is coming to an end.

“On the surface, the underlying outlook for the global economy remains supportive for equities but there are a number of factors which lead us to expect a ‘pause’ in markets over the coming months,” Godding explained. “These centre on a fading credit impulse and fiscal stimulus in China and cooling global credit conditions.

“Chinese credit expansion has been an important driver both of its domestic growth but also globally, with a notable influence on manufacturing output and raw material prices - which in turn impacts inflation. Since mid-2016 Chinese authorities have been striving to reign in credit growth and restrain the shadow banking system. The data appears to suggest a typical lag effect of around eight months between Chinese credit growth and its impact on manufacturing output, so we expect the weakening Chinese credit growth to manifest itself in slower output in the second half of this year before starting to recover again in 2018.

“The tone from central banks, including the Bank of England and European Central Banks, has also shifted recently. While policy remains accommodative, central banks have collectively adopted a more hawkish tone and by acting in unison, have provoked a significant sell-off in sovereign bonds and steepening of the yield curve. With inflation in most parts of the world rolling over, in part due to renewed weakness in energy prices, the outlook is therefore one which holds the prospect of simultaneous but probably modest monetary tightening in the face of high debt levels, subdued core inflation and weakening credit growth.

“This is not a compelling environment for bond markets and in our view these offer no margin for safety. While the case is more constructive for equities and politicians are under pressure to step up to the plate with greater fiscal stimulus measures, sustainable economic growth requires rising real wages. That would be healthy for economic growth but higher costs could also prove a drag earnings growth.

Equities are ‘fair value’

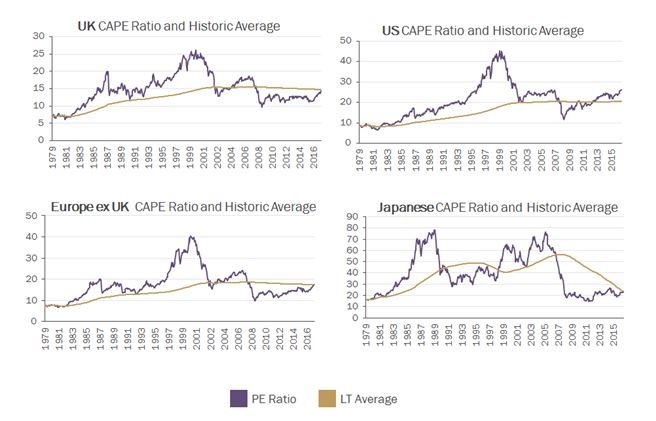

With key market indices hitting new highs and very low levels of volatility, it is understandable that there is a lively debate among professional investors and commentators as to whether equities are now too expensive. Godding argues: “While there are clear signs of euphoria in parts of the market, notably technology, which has been a key factor in driving US equity multiples to the upper end of historic trend, valuations do not look excessive for most regions compared to long-term trends and are actually quite compelling for Asian and emerging market equities. The step up in bond yields at the end of June has had a knock-on impact, with a decent correction in consumer staples which had been trading on very high multiples and interest rate sensitive stocks such as utilities, real estate and telecoms.

“We therefore see an environment where the risk/return trade-off for sovereign bonds is poor and investors looking for lower risk assets in a portfolio might instead use absolute return funds with low volatility strategies. We are more constructive on equities and less concerned about current valuations than some other investors. But we do anticipate developed equity markets are unlikely to move materially higher in the near term until there is evidence of renewed earnings growth or bold fiscal initiatives. Within our overall neutral view of equities we continue to have a preference for Europe amongst developed markets and also favour Asia Pacific and Emerging Markets.”

- ENDS -

*In the six months to end of June, the MSCI UK index has delivered a total return of 6% in Sterling terms, while the US S&P 500, MSCI Europe ex UK and Japan’s Topix indices respectively returned 4%, 12.6% and 6%. The greatest returns in the first half however came from emerging markets and the Asia Pacific region, with the MSCI Emerging Markets and MSCI Asia Pacific ex Japan indices surging 12.8% and 14.1% in total return terms.

Important Information

The value of investments, and the income derived from them, can go down as well as up and you can get back less than you originally invested. Past performance is not a guide to future performance. This article does not constitute personal advice. If you are in doubt as to the suitability of an investment please contact one of our advisers. Current or past yield figures provided should not be considered a reliable indicator of future performance.

Disclaimer

This release was previously published on Tilney Smith & Williamson prior to the launch of Evelyn Partners.