Common complex financial instruments in the technology industry part 2

2020 has been a bizarre and unreal experience. However, despite this turbulence, the technology industry has shown incredible resilience while driving innovation. Other industries have suffered from the impacts of the coronavirus (COVID-19) pandemic but businesses in the technology sector were not as heavily impacted.

Part 2: Different classes of shares

In a nutshell

There are many reasons for having different classes of shares or preference shares. One of the most common reasons is when a party invests into a business, as shareholders can agree what rights each shareholder should and should not have. From a company law perspective these are shares, but the complexity arises in the world of accounting, as a single word change in a share agreement can result in these shares being classified as a liability.

Clearly different classes of shares are very useful tools for ensuring that the structure of the company suits each of its shareholders and allows the smooth running of the company. However, there could be significant accounting implications such as recognition of large fair value movements year on year thereby impacting profit or loss.

In this article we focus on practical issues relating to preference shares or preferred ordinary shares that are settled in an entity’s own equity instruments.

Overview

It is important to understand the terms underpinning each class of shares. The articles of association is a good place to start, however, other investors / side agreements may impact the accounting of these shares.

Essentially, the accounting standards require an issuer of a financial instrument to classify the financial instrument, or its component parts, as a financial liability or as equity in accordance with the substance of the contractual arrangement and the definitions of a financial liability and an equity instrument. Whilst UK GAAP is not as prescriptive as IFRS, the principles underpinning both standards are fundamentally consistent.

The overriding principles state that when the issuer does not have an unconditional right to avoid the obligation to deliver cash or another financial asset and the contract does not, in substance, evidence a residual interest in the net assets of the issuer after deducting all of its liabilities, then the instrument is not an equity instrument.

Smith & Williamson view:

The most common types of shares we see classified as liability or compound instruments (combination of both liability and equity components) are in relation to preference shares or preferred ordinary shares. Preference shares are often issued as a means of raising capital, without diluting the voting power of the ordinary shareholders. To compensate for the loss of voting power, the shares will often have preferred rights over the ordinary shares, such as fixed dividends and/or redemption rights, as well as preferences on liquidation.

A key consideration over classification is to really understand the substance of the contractual arrangement, rather than its legal form. The most common classification error we see arise is in relation to preference shares that are settled in the entity’s own equity instruments.

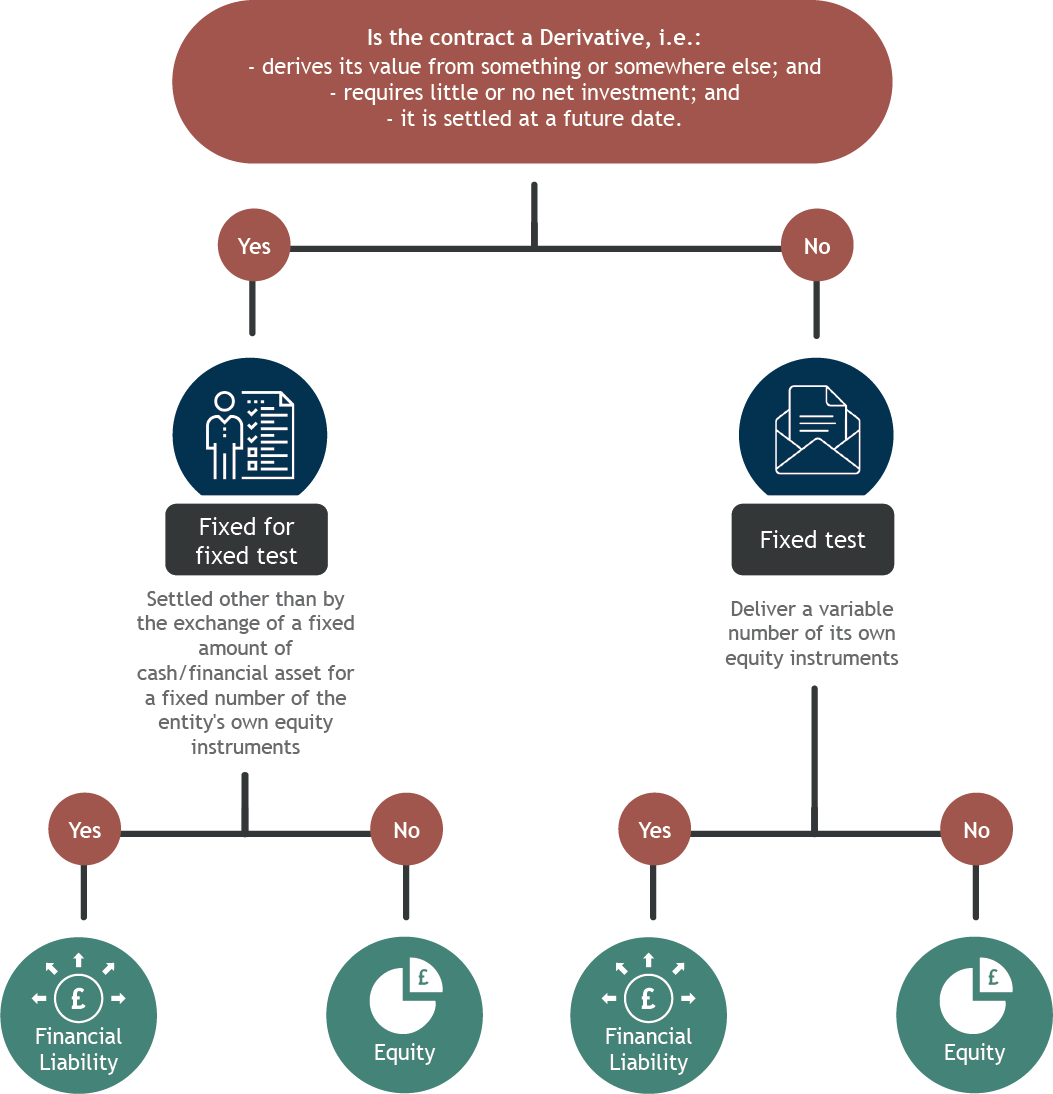

Fixed test or fixed-for-fixed test?

Where preference shares have the same attributes as ordinary shares and there is an option for them to convert into ordinary shares, then there is some debate over the appropriate accounting treatment. The debate centres on whether the “fixed” or “fixed for fixed” test is applied. The IASB has tentatively decided to explore issuing clarifying amendments to IAS 32 Financial Instruments : Presentation, but we suspect this will take a number of years.

Below is an illustration relating to the classification of financial instruments settled by issuance of the entity’s own equity instruments.

In addition to the above, if preference shares are non-redeemable, there is a need to look at the other clauses or rights attached to the instrument. For example, if the distribution to preference shareholders is at the discretion of the issuer, this may indicate that the preference shares are equity instruments. Alternatively, if distributions are mandatory, this may result in a financial liability instrument as the company cannot avoid the obligation to deliver cash or another financial asset.

Compound instruments

The terms of the financial instrument may be structured as such that it contains both an equity and a liability component (i.e. the instruments are neither entirely a liability nor entirely an equity instrument).

An equity instrument is any contract that evidences a residual interest in the assets of an entity after deducting all of its liabilities. The liability and equity components of a compound instrument are required to be accounted for separately and must be classified in accordance with its substance rather than its legal form.

Equity features in a preference share instrument which breach the fixed test or fixed for fixed test (resulting in a compound instrument) may include:

- Instruments with rights to a fixed minimum dividend and additional discretionary dividends

- Instruments with fixed dividend rights but with the right to share in the residual net assets of the issuing entity on the entity’s liquidation.

Practical implications to be aware of:

single word may change the accounting of these financial instruments completely. Existence of other side agreements that directly impact the conditions relating to the preference shares may also change the accounting of these financial instruments. As a result, the accounting treatment and subsequent valuation may differ significantly. Below are common implications:

1. Anti-dilutive features

Many anti-dilutive provisions are structured so as to avoid any loss of value if certain events occur such that the holder of the instrument remains in the same position relative to existing ordinary shareholders before and after the event. We consider such provisions to not breach the fixed-for-fixed criterion. If the adjustment to the conversion ratio applied only to the preference shareholder and not to the existing ordinary shareholders, this feature may result in a financial liability.

2. Down-round protection

Under these arrangements the number of shares increases if the strike price of the conversion option is adjusted downwards or if the shares are subsequently issued at a lower price. These are protection features against adverse movements in share price at the expense of ordinary shareholders. There is a significant debate as to whether this results in a liability instrument. Generally, if these clauses are at the expense of the ordinary shareholders, these are liability instruments. However, management will also need to consider whether the entity can avoid the down-round clause from being activated by not issuing shares below the conversion price – thereby challenging whether the entity has an obligation to issue variable shares. This may result in a different conclusion over the accounting classification. Interestingly, under US GAAP (ASC 815-40), down-round protections may result in an equity classification.

3. Variable number of shares

The following are common clauses we see that do not meet the definition of an equity instrument:

the number of shares to be delivered on settlement is based on a sliding scale that reduces as the share price increases

- conversions into ordinary shares not priced in the functional currency of the entity

- change of control clauses that enhance the rights of preference shareholders against all other shareholders through a conversion formula

- variations in exercise price or prices dependent on the profits or the value of an underlying asset such as a commodity, market price or security.

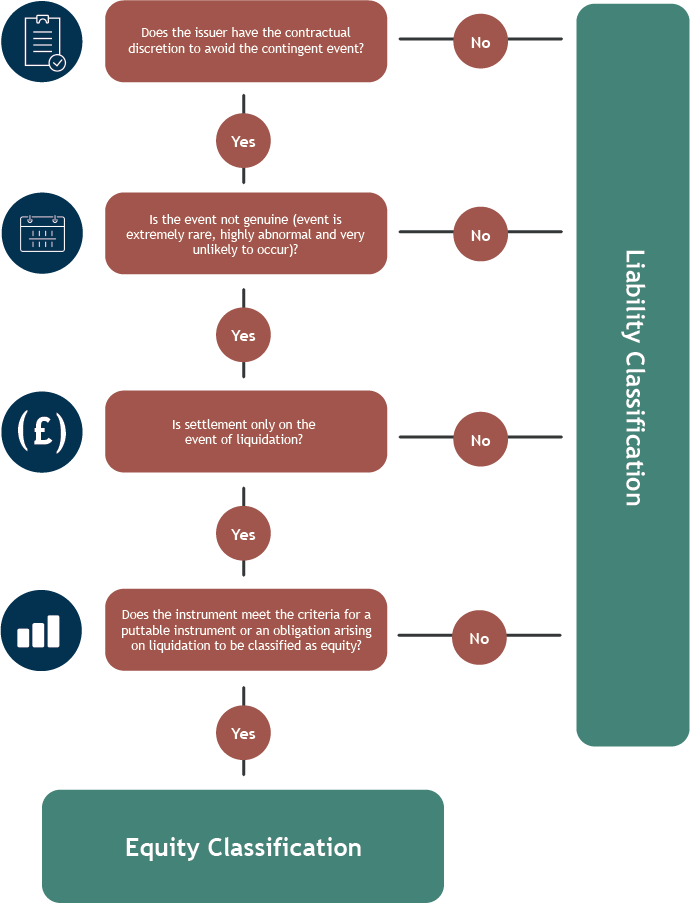

4. Contingent Settlement provisions

There may be an obligation to deliver cash or other financial assets on the occurrence or non-occurrence of uncertain future events that are beyond the control of the issuer and holder of the instrument such as a change in a stock market index, issuer’s future revenues or net income. Classification as either equity or liability is illustrated below:

Smith & Williamson view:

Preference shares that can only be settled by issuance of an entity’s own equity instruments (e.g. ordinary shares) are not necessarily equity instruments.

We note that there are many variables and clauses dictating the terms of preference shares and it is imperative that management does not make assumptions without collecting all the facts as well as understanding the substance of the transaction.

Ultimately, if deemed a liability the business is potentially transferring its value from existing ordinary shareholders to the preference shareholders and this represents a cost to the business. As a result, there could be significant movements year on year in an entity’s financial statements.

Valuation considerations

It is important to understand the particular circumstances of the business and the rights attached to preference shares as these may have significant valuation considerations. Below are a few areas to consider:

Valuation - If preference shares are deemed non-basic financial instruments under UK GAAP or financial liabilities there may be a need to fair value these instruments. Fair value may change over time and have a significant impact to a company’s financial position. Further complexities arise in estimating the fair value as the company may need to consider its overall enterprise value and the corresponding allocation of this value to senior debt, if applicable.

If preference shares are deemed compound financial instruments, on initial recognition the equity component of the compound financial instrument may be determined as the residual amount after deducting the fair value of the financial liability component. The fair value of the financial liability may be determined as the present value of the future contractual stream of cash flows discounted at a rate of interest applied at the time by the market to a similar instrument with comparable credit status and providing substantially the same cash flows on the same terms but without the right to the discretionary dividend cash flows.

Management may need valuation support to address the judgements above.

Return on investment – The dividends receivable on the preference shares should be compared to an appropriate market rate of return for such an investment. Any corresponding impact on value will also have to take into account whether the preference shares are redeemable and the expected time to redemption.

Smith & Williamson view

The valuation of preference shares can vary over time as the company’s circumstances and market conditions change, which could lead to a significant impact to the company’s profit & loss account and balance sheet. External advice should be sought where this is a key and complex judgement in the accounts.

DISCLAIMER

By necessity, this briefing can only provide a short overview and it is essential to seek professional advice before applying the contents of this article. This briefing does not constitute advice nor a recommendation relating to the acquisition or disposal of investments. No responsibility can be taken for any loss arising from action taken or refrained from on the basis of this publication. Details correct at time of writing.

Nexia Smith & Williamson Audit Limited

Registered to carry on audit work and regulated by the Institute of Chartered Accountants in England and Wales for a range of Investment business activities. A member of Nexia International.

Smith & Williamson LLP

Regulated by the Institute of Chartered Accountants in England and Wales for a range of investment business activities.

Smith & Williamson LLP is a member of Nexia International, a leading, global network of independent accounting and consulting firms. Please see https://nexia.com/member-firm-disclaimer/ for further details.

Smith & Williamson LLP is part of the Tilney Smith & Williamson group.

Registered in England No. OC 369631.

Tax legislation is that prevailing at the time, is subject to change without notice and depends on individual circumstances. Clients should always seek appropriate tax advice before making decisions. HMRC Tax Year 2022/23.

Ref: 108021eb Exp: 30/09/2022

Disclaimer

This article was previously published on Smith & Williamson prior to the launch of Evelyn Partners.