Why does the UK's construction industry not capitalise on R&D tax credits?

Lack of awareness has hindered take up of a valuable tax relief for both SMEs and larger operators

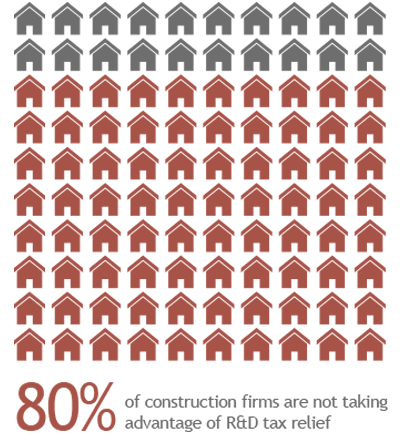

Estimates put the value of R&D eligible for tax relief in the UK’s construction industry at £1 billion, but claims have averaged just £23 million a year. What are R&D tax credits and how can UK construction companies claim them?

From developing new materials, to overcoming logistical challenges, research and development (R&D) is happening within construction businesses across the UK on a daily basis.

Yet when it comes to claiming R&D tax credits for that innovation, construction firms are missing out on a valuable tax break that could either reduce their corporation tax liability, or result in cash back from HMRC. In 2014-15, only 480 R&D claims were made by construction companies, out of a total 290,000 claims submitted. What’s more, Smith & Williamson’s recent property and construction survey found that almost a quarter of construction companies had never even heard of R&D relief, let alone applied for it.

What are R&D tax credits?

R&D tax credits were essentially designed as a tax incentive to promote innovation in UK industry. The incentive is increasingly being pushed as a way not only to increase companies’ investment in R&D, but to strengthen UK enterprise in the run up to Brexit. In last year’s autumn budget, Philip Hammond announced a £2bn increase in spending on the initiative by 2020/21.

For the construction industry, it’s estimated that eligible R&D could be worth over £1 billion in tax credits annually – and that’s assuming that innovation accounts for just 1% of the sector’s turnover. Recently, the sector’s R&D tax credits claims have averaged just £23 million per year.

Source: Invennt

Why construction are companies missing out

Almost every industry in the UK is failing to claim the full R&D tax credits it is eligible for. The reasons for this are varied; some businesses are unaware of the scheme, some are put off by the time-consuming nature of applications and some think that research and development is the preserve of ‘lab coats’ in technical and scientific fields.

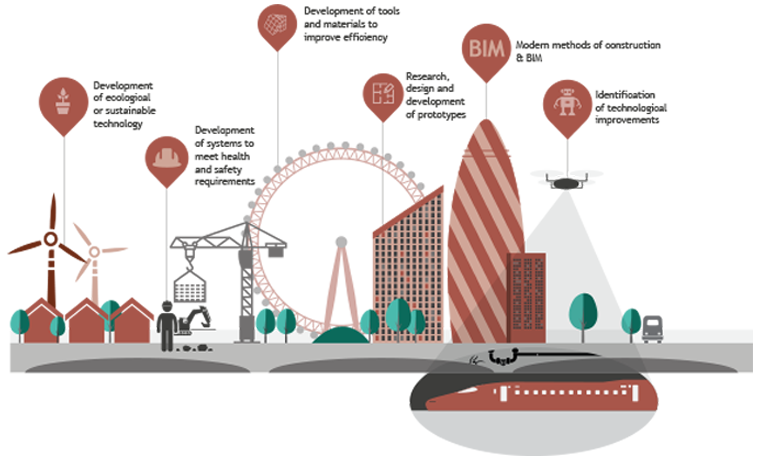

The story is no different for the construction sector. Lack of awareness is a problem, but the more prevalent concern is that many in the sector consider their work to be outside of the R&D remit. Yet the relief is designed to encourage innovation across every sector, not just science.

In construction, eligible R&D can include anything from updating safety processes to developing a new technique, and a wide range of other activities in between. As these activities usually form part of various departments, as opposed to being restricted to a dedicated research and development department, defining related expenditure can be difficult for those without the right experience.

Making R&D easier

There are companies who have attempted to claim in the past, only to be met with a long, complicated process that resulted in little reward at the end of it. This is often enough to deter many businesses from trying again: most are keen to get started with their next project, rather than spend time writing a detailed report for HMRC.

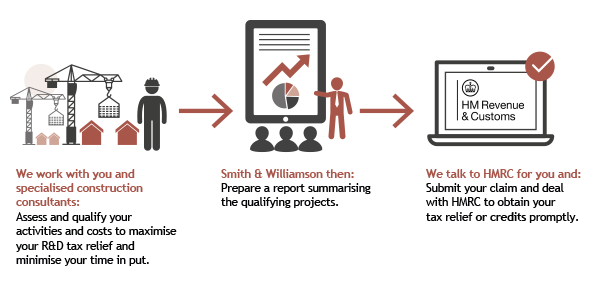

However, R&D activity and expenditure can be difficult to spot, even for an accountant, and claims can underestimate both the R&D that has been carried out and the expenditure attached to it. With specialist assistance, R&D claims can be hugely beneficial. An R&D tax credit specialist will work alongside a business and its accountant, identifying eligible R&D to maximise the claim’s potential.

Larger companies and SMEs can both benefit

The scheme is open to both SMEs and larger businesses, but the rules and benefits differ for both. SMES can use the relief to reduce their tax liability, receive a cash repayment, or offset losses. For large companies, R&D tax relief can provide a tax credit against their corporation tax of 10% of qualifying expenditure. To find out more about the cash benefits of making an R&D claim, and how Smith & Williamson can assist in making a claim, visit our FAQ page.

DISCLAIMER

By necessity, this briefing can only provide a short overview and it is essential to seek professional advice before applying the contents of this article. This briefing does not constitute advice nor a recommendation relating to the acquisition or disposal of investments. No responsibility can be taken for any loss arising from action taken or refrained from on the basis of this publication. Details correct at time of writing.

Disclaimer

This article was previously published on Smith & Williamson prior to the launch of Evelyn Partners.